Brent’s Balancing Act

Since the front-month Brent futures hit a three-year low of almost $68.50/bbl on 05 Mar, the M1 contract has steadily ticked up to $71.30/bbl by the time of writing on 17 Mar. The market had largely been in a period of bullish consolidation around the $70/bbl level last week, with traders navigating a variety of both bullish and bearish factors influencing crude oil prices. We now anticipate this moderate support to continue in the short-term, with the potential for price to end the week between $70 and $73/bbl.

The following factors are expected to be key drivers of price action this week:

- Geopolitical risk in the Middle East and Russia-Ukraine conflict

- Positive China macroeconomic data

- Risk takers rebuild net long positions

Over the weekend, the US carried out a wave of airstrikes on the Iran-aligned Houthi rebels in response to renewed threats to attack international vessels in the Red Sea. At least 53 people have been killed so far, with US defence secretary Pete Hegseth stating the airstrikes will continue indefinitely until the Houthis stop firing on US ships. Although this may not cause much physical disruption to supply flows, with very few oil tankers journeying through the Red Sea in recent months, these latest attacks are a strong sign that tensions between the US and Iran could heat up. Iran has already rejected invitations for nuclear talks with the US, in addition to fresh sanctions being imposed on Iran’s Oil Minister Mohsen Paknejad last week. While it remains to be seen whether these developments are a prelude to maximum pressure policy on Iran, in the meantime, they are helping to raise risk premia in oil prices. Similarly, the situation in the Russia-Ukraine conflict is no better, despite continual efforts from the US to bring about a ceasefire. Last night, a Ukrainian drone attack targeted energy facilities in Russia’s Astrakhan region, sparking a fire. This followed a series of drone strikes on Russian energy infrastructure last week, with the 11 Mar attack on the Druzhba pipeline temporarily disrupting Russian oil supplies to Hungary. The Druzhba pipeline is a key supply route for much of central Europe and the attack demonstrated that Ukraine could still significantly impact Russian oil flows.

China’s economic prints surprised the upside, potentially a reflection of the government and central bank’s stimulus efforts last year. China’s Jan-Feb retail sales rose 4% y/y compared to a forecast of 3.8%, while fixed investment and industrial output rose by 4.1% y/y (est. 3.2%) and 5.9% y/y (est. 5.3%), respectively. Moreover, China’s government has announced further measures, including plans to revive consumption by boosting incomes and stabilising the stock and real estate markets. Investors have reacted positively to the plans so far, as the CSI 300 benchmark stock index rallied the most in two months last Friday. If the economy is now set on course for the government’s ambitious 5% growth target for 2025, China’s oil demand growth prospects will still face challenges from the electrification of its car fleet and the shift from diesel to gas in trucking.

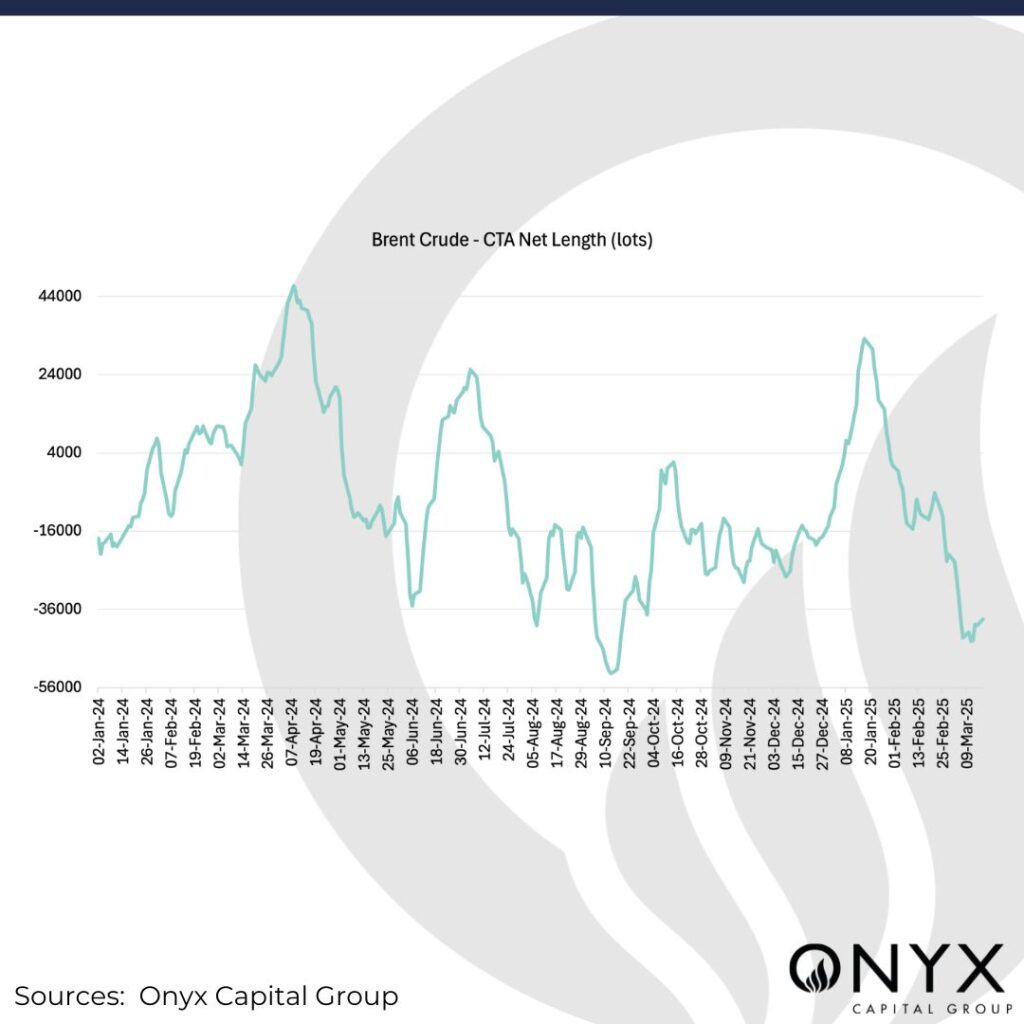

Finally, ICE COT data for the week to 11 Mar shows that positioning has become more bullish w/w but remains risk-off overall. Speculative players removed 17mb (-14% w/w) from their short positions in the week to 11 Mar, compared to a proportionally smaller decrease of 26mb (-9% w/w) in long positions. CTA net positioning in Brent also is becoming less bearish, moving from -44k lots on 12 Mar up to -38.5k lots on 17 Mar. As a result, there is room for bullish momentum to pick up this week, however, we will need to see a strong bullish catalyst to cause any significant reaction in the market. Any unexpected announcement from Trump surrounding US tariffs could quickly lead to crude oil prices correcting lower.