Welcome to our Live Blog of what is driving oil and other markets throughout the day.

If you hear otherwise, let us know at insight@onyxcapitaladvisory.com

Morning Macro 16 May 2025

US Retail sales grew 5.2% y/y in April and PPI printed in deflation in April at -0.5% m/m (Core -0.4%). Labour market still robust: weekly initial jobless claims as expected. Fed should be on hold for longer, with OIS now pricing 59 bps cut by year end – up from 50 bps priced couple of days ago but much lower than pre-FOMC last week.

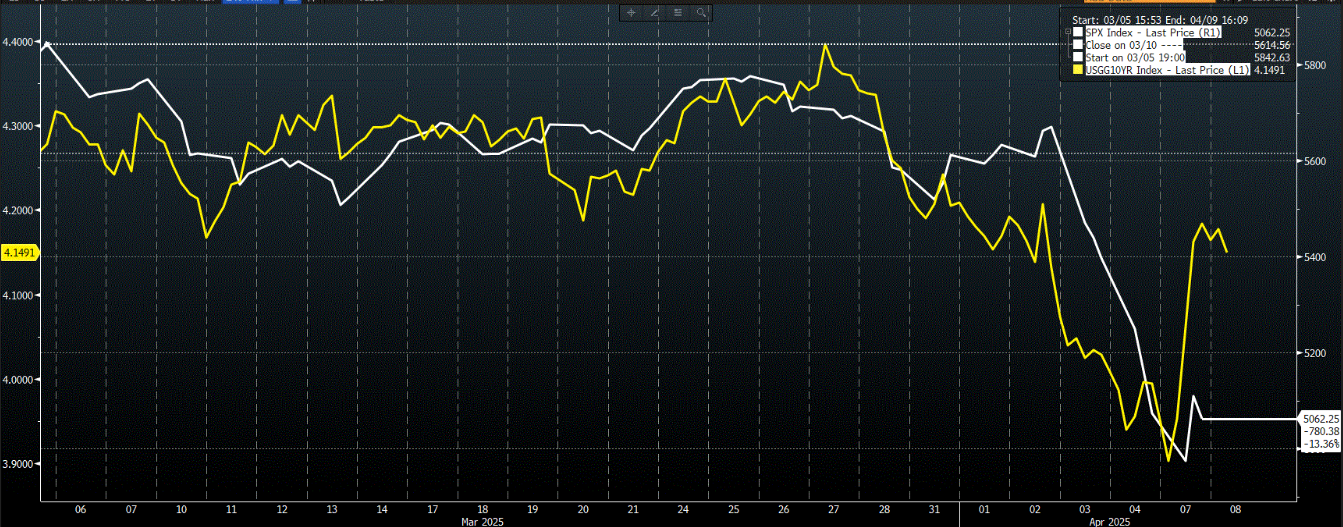

Gold bounced back off 50-day moving average from below $3.2k/oz, but still down over 8% from ATH. Trump: would prefer to pay off debt before building wealth fund. Little surprise: US 10-year treasury yield fallen back from yesterday’s high but still elevated at 4.40%. But Trump’s approval ratings increased slightly to 44% according to a recent Reuters/Ipsos poll. As trade deals and tariff reductions come in, Americans are less concerned about recession but 69% still said they are. It’s easy to feel less pessimistic when stocks are up – S&P 500 now at highest since early March, up over 22% from 7 April low.

However, Walmart warned it will pass on additional tariff costs to customers, as even the reduced tariffs are too high for them to “absorb all the pressure” of increasing costs. Following trade war reprieve on the weekend, PBoC fixing of yuan has strengthened and USD/CNY now trading at 7.200.

Data today: US Housing Starts

Morning Macro 15 May 2025

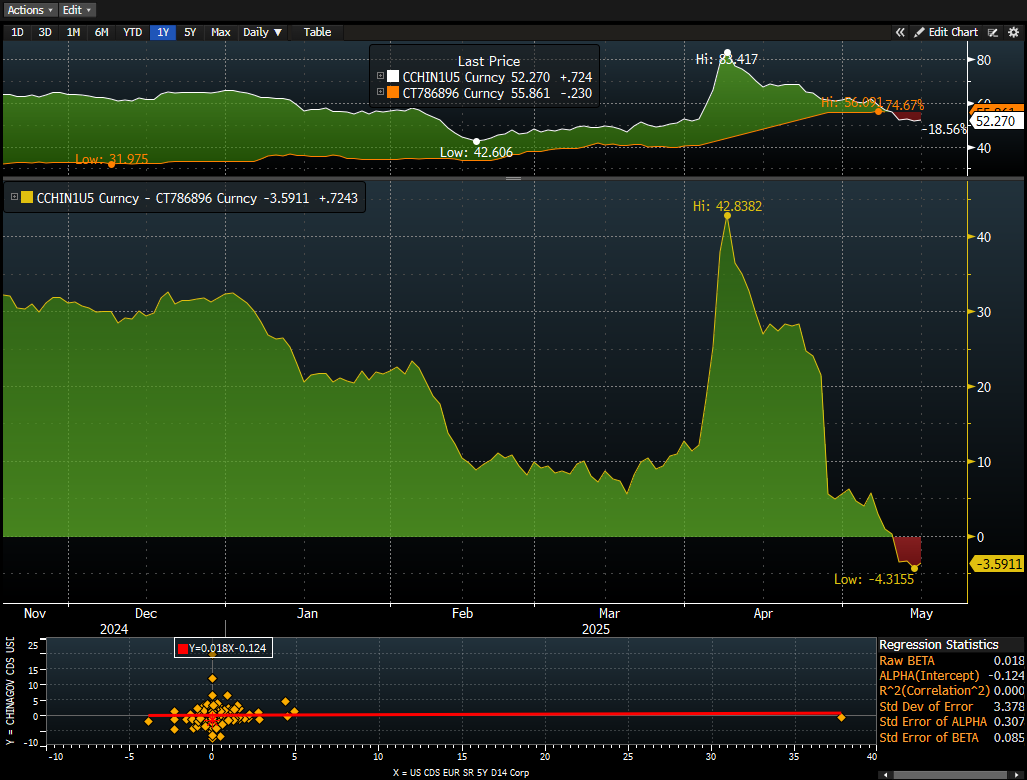

For the first time in history CDS on US treasuries are trading above those on equal maturity CGBs (Firgure 1). The market is pricing a higher risk of sovereign default in the US than in China! DOGE is not working and year to date interest payments on treasury debt securities now stands at $684 billion, up almost 10% y/y. No wonder Trump’s keen for the Fed to cut. In contrast risk premium on China local corporate bonds at record lows following latest PBoC easing.

Meanwhile Optimism around China is growing. Morgan Stanley bumped up their GDP forecast in China this week to 3.7% – 4%, up from 3.4%. But not all plain sailing in China, New Yuan Loans were soft in April at only 280 bn yuan, compared with consensus of 700 bn yuan and a prior of 3640 bn yuan… appetite for credit is still not there. Outstanding loan growth slowed to 7.2% y/y, down from 7.4% y/y last month. Total Social Financing also slowed from 5.8 tn yuan in March to only 1 tn yuan in April.

UK GDP stronger than expected at 1.3% y/y for Q1, albeit slowing from 1.5% in 4Q24. UK March industrial production down at -0.7% m/m, reversing +1.7% in Feb.

Boeing stock up almost 60% since the start of April. Yesterday Qatar Airways agreed to a massive 160 aircraft deal with Boeing for 777X and 787’s worth $96bn. Elsewhere in equities, Tencent revenues were up 13% over the first quarter of 2025.

Gold broke support at $3220, now trading around $3143.60 at the time of writing. (Figure 2)

Data today: US PPI, US Retail Sales, US Industrial Production

Morning Macro 14 May 2025

U.S. CPI rose 0.2% m/m in April, below the 0.3% consensus and reversing March’s deflation. Core inflation matched headline m/m, while y/y core held steady at 2.8%—still above the Fed’s target. Headline y/y inflation eased to 2.3% from 2.4% in March.

No reason for pivot at the Fed here – market’s realising higher for longer: OIS now pricing -54bps by year end, from -102 at end of April. Don’t fight the Fed! Yields up off Fed expectations, with a flattener in the curve.

China’s vehicle sales rose 9.8% y/y in April 2025 to 2.59 million units, up from an 8.2% gain in March, according to CAAM. New energy vehicles (NEVs) surged 44.2% to 1.226 million units, making up 47.3% of total sales.

Auto production in China is still booming. China built 10.1 million units in the first four months of the year, up 12.9% y/y. Sales were also >10 million units, up 10.8% y/y, the first time both have exceeded 10 million. Stimulus, such as consumer repurchase purchase programmes is passing through. Oh and China just reported their largest two-month change in copper imports in history!

Germany ZEW economic sentiment index surged to 25.2 in May, rebounding from April’s near 2 year low. Optimism in Germany for once? Formation of a new government, tariff progress and some signs of inflation stabilising helped. But current conditions fell 0.8 points to -82!

US equities continued to rally on trade deal news. With core indices having eroded liberation day losses. Relative to April 2, Nasdaq no +8.3%, SP500 +3.8%, Russell 2000 +2.8%. Risk on, and gold now testing support, double top looks like a precarious set up!

No key data today

Morning Macro 13th May

The market flips back into euphoria mode on the tariff news with recession odds plummeting. However the market seems to overlook that tariffs are still the highest level since 1930. (Chart 1, The Budget Lab, @PeterBerezinBCA)

GOLDMAN NOW SEES NEXT FED RATE CUT IN DECEMBER INSTEAD OF JULY – Bloomberg

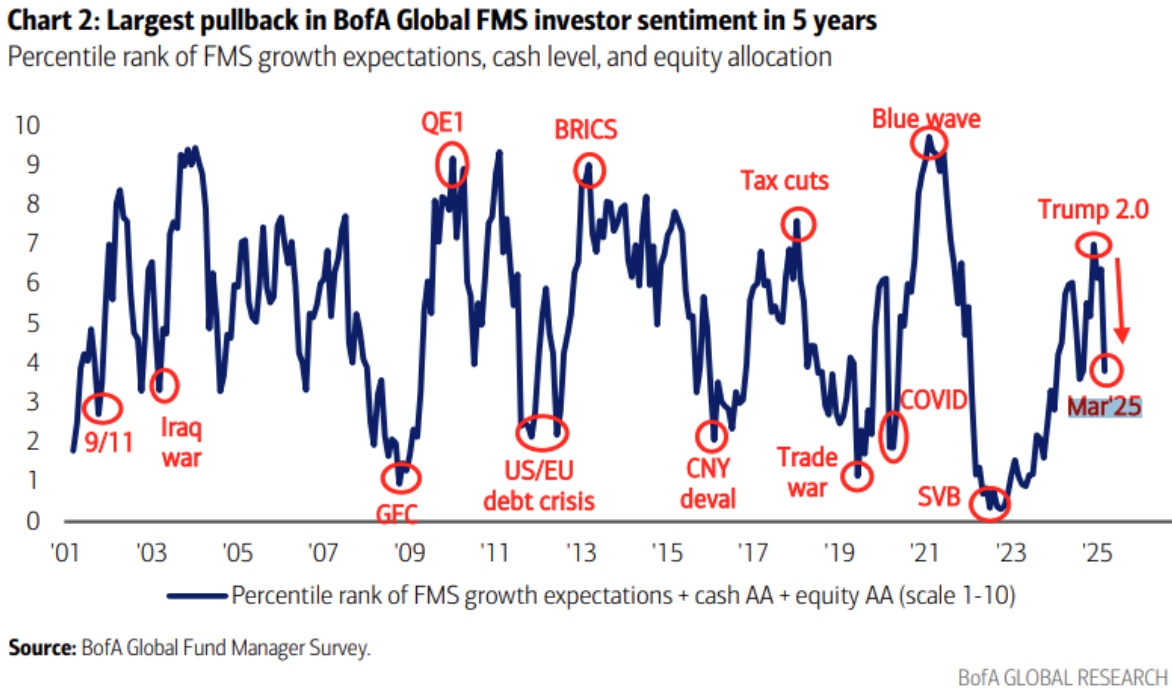

Recession expectations have peaked per Bank of America Global Research (Chart 2), and Polymarket have the chance of US recession in 2025 falling 11% yesterday to 39%.

However gold appears to bounce on good support after it’s 3rd largest drop on record. Clear support at $5237 (Chart 3, Trading View)

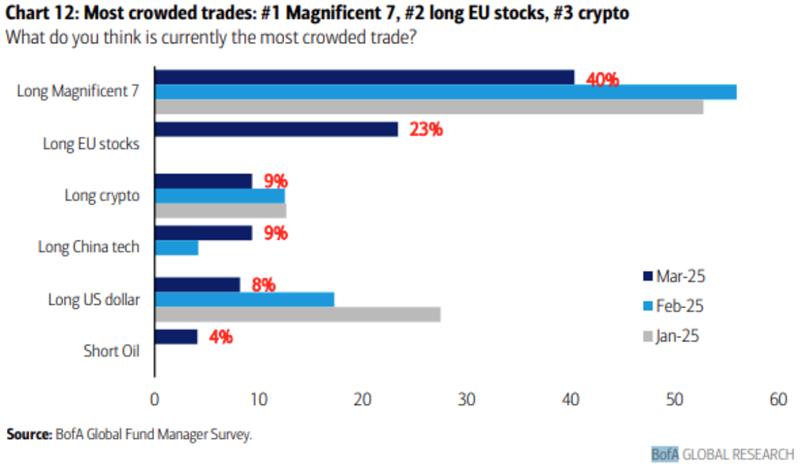

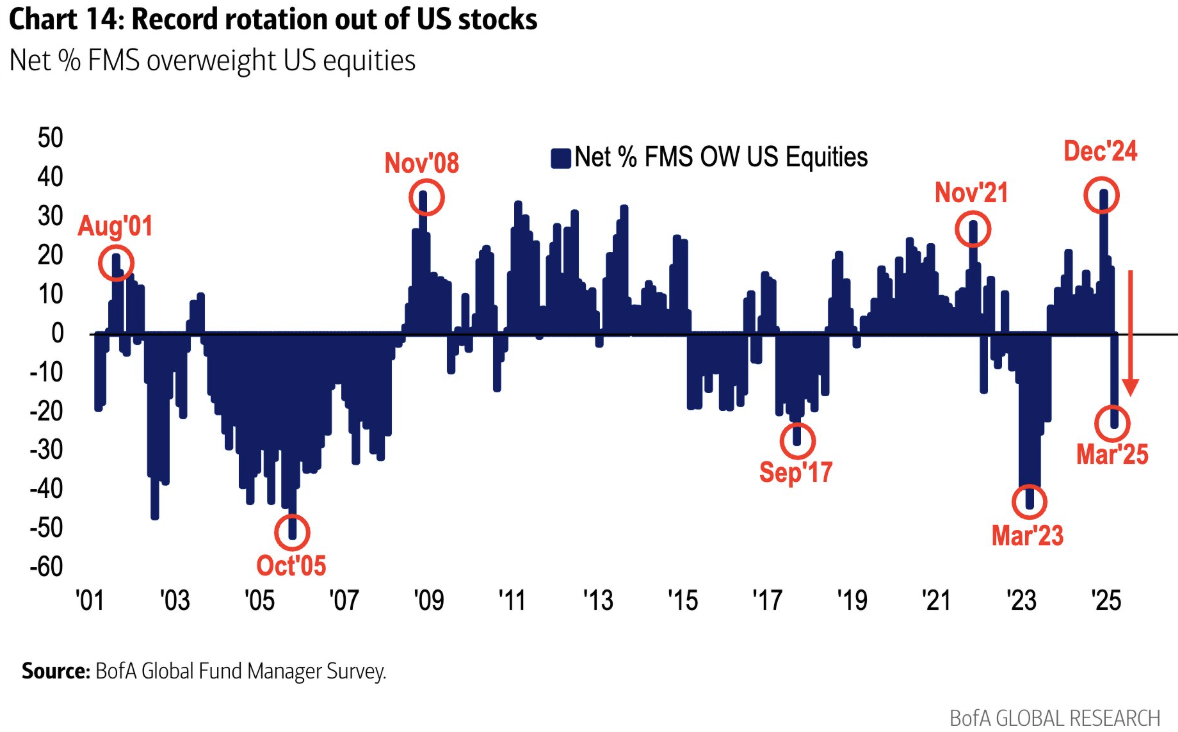

BofA Fund Manager Survey: Fund Managers most underweight US Dollars since 2006…..with equities surging past their Liberation Day levels we could see more of a short squeeze on dollar positioning here.

Buying stocks? …. Errrrmmm….. Citi U.S. Earnings Revisions Index has been negative for 20 consecutive weeks (Chart 4, Bloomberg)

UK unemployment rate rises from 4.4% to 4.5%

Coinbase jumps 5% on announcement that it is to join the S&P500. S&P ETFs are forced to buy.

Data today -US CPI (estimated 2.4$ yoy, 2.8% core, both same as last time), German ZEW confidence

Morning Macro 12th May

Headlines just out a substantial de-escalation in US-China tariff negotiations, but with the 20% Biden tariff the effective tariff rate on China is still about 50%. Yes, this is a major de-escalation, but we are not going back to what it was before Trump. Gold immediately sells off -2.8%, Brent jumps +2.7%, US 2yr yield jumps+10bp, S&P500 +3% (and above Liberation Day levels!).

News out that President Trump will be signing an Executive Order today to reduce drug prices by 30% to 80%……. RIP Biotech.

With Bitcoin surging to $105k, ETH is now up over 40% in less 3 days.

Japan’s 40-year bond yield just jumped to its highest level in 2 decades.

Data this week –

Tuesday – US CPI, Australian & German consumer confidence, K employment,

Wednesday – German inflation

Thursday – US PPI, retail sales, Philly Fed, Fed Chair Powell speaks, Australian employment, UK IP, French inflation

Friday – Japan GDP, Michigan Consumer confidence

Morning Macro 9th May

New York Post is now reporting that U.S. is planning to cut Chinese tariffs from 145% to 50%.

Bank of England cut 25bp to 4.25% as expected. However, the vote split is what is raising eyebrows. Dhingra and Taylor voting for a 50-bps rate cut is somewhat expected but both Mann and Pill voting for the bank rate to be unchanged is the standout here.

U.S. ISSUES NEW IRAN-RELATED SANCTIONS -U.S. TREASURY WEBSITE

China’s exports surged by 8% in April, above the consensus forecast of 2% and despite a 21% drop in sales to the US. This surge comes as China redirects more of its exports to other countries, which is likely to exacerbate concerns about the adverse implications for certain domestic industries.

UK and the United States have agreed terms for a tariff trade deal, with the British government agreeing to concessions on imports of American food and agricultural products in exchange for lower tariffs on British car exports.

A day of Trump quotes, the market is becoming tone deaf to them….

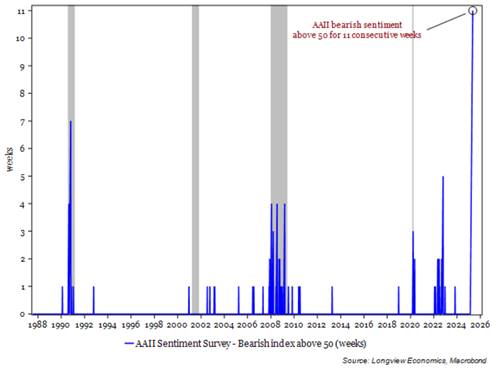

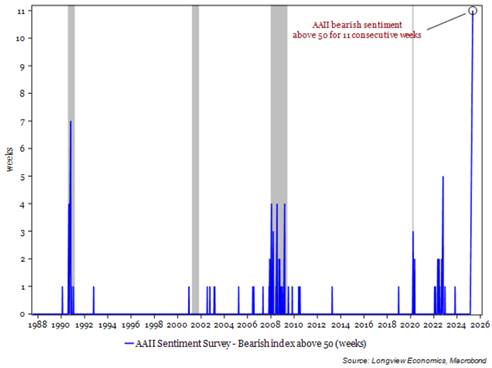

Do as I do, not as I say! Despite record retail purchases of US equities, retail sentiment is still BEARISH, despite a 19% rally in the SPX since early April. The ‘AAII bears’ index has now been above 50 for 11 weeks…. Longest stretch on record. Chart 1, Longview economics, Macrobond)

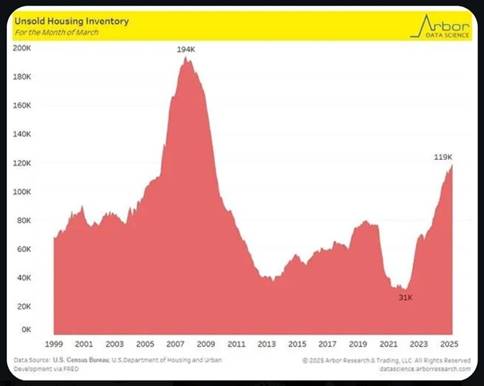

US unsold housing inventory is at its highest levels since the financial crisis (Chart 2, US census bureau, US department of housing & urban development, Arbor dada science).

While mortgage rates are finding a new range between 6-8% for this cycle … rivals range seen in mid-to-late-1990s (Chart 3, Bloomberg)

Japan wage shock: Real wages plunge to -2.1% YoY, the worst in two years, and a deflationary disaster for the BOJ which puts a final nail in any hiking plans.

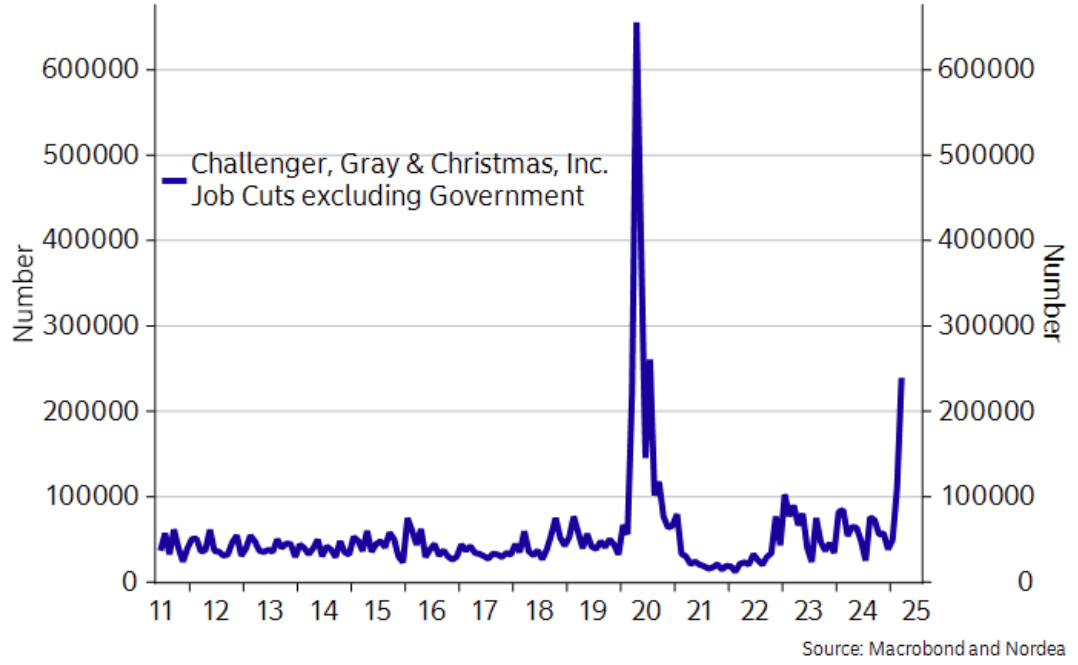

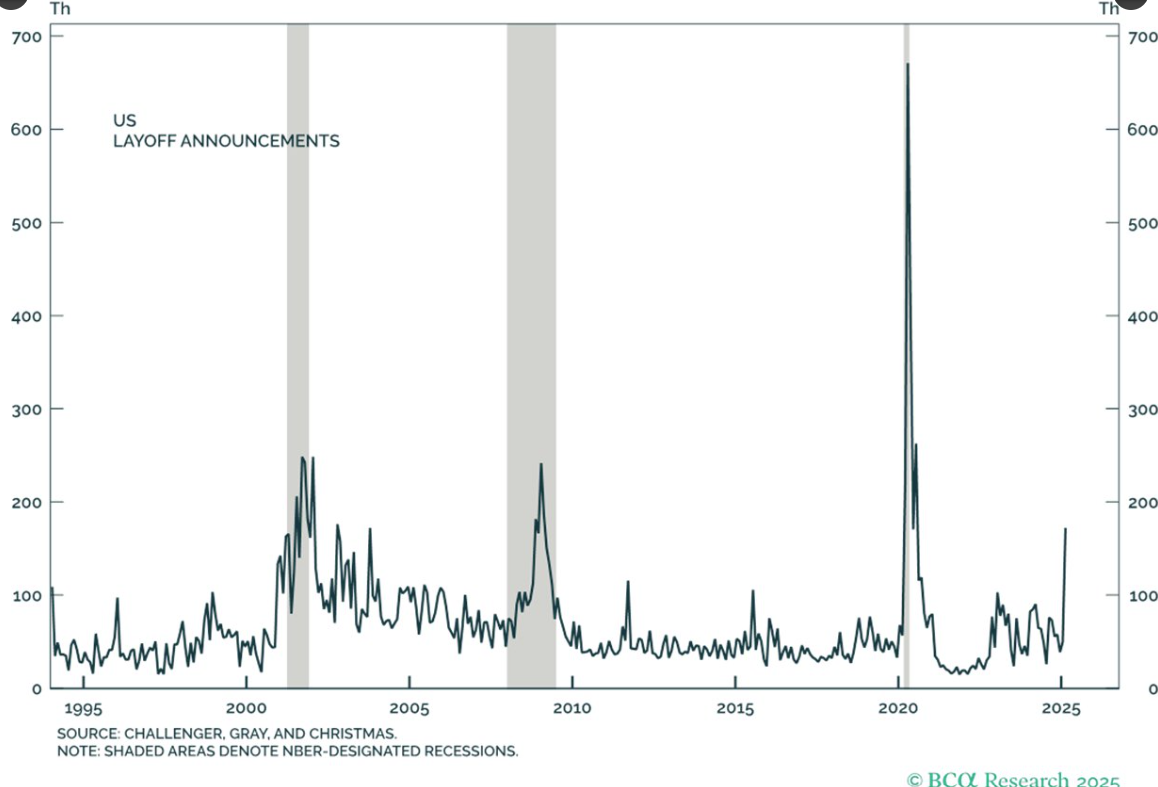

Despite continued strong hard data, US layoffs are surging US employers announced 105,441 job cuts in April, the highest for any April in 5 years. Excluding 2020, this was the highest count for any April since 2009. Over the last 6 months, there have been 699,012 job cuts, the most since the 2020 pandemic. (Chart 4, LSEG Datastream, Challenger, Gray & Christmas, Kobeissi Letter)

Only data today – Canadian employment

Morning Macro 8th May

The US dollar rallied and gold sold off as Fed Chair Powell fought back against OIS market pricing aggressive rate cuts. In his FOMC press conference he said ‘wait and see’ 12 times and ‘wait’ another 13!….. He did also say however that Trump’s tariffs will lead to increased inflation, a slowdown in economic growth and higher unemployment. He also said debt is on an unsustainable path.

Trump announcement at 10pm EST (rumours of a US-UK trade deal)

Gold lower and looks ominously like a short -term double top is in place. Expect more profit taking.

Goldman Sachs now expecting 4% inflation by Christmas, led by 6-8% inflation in goods prices.

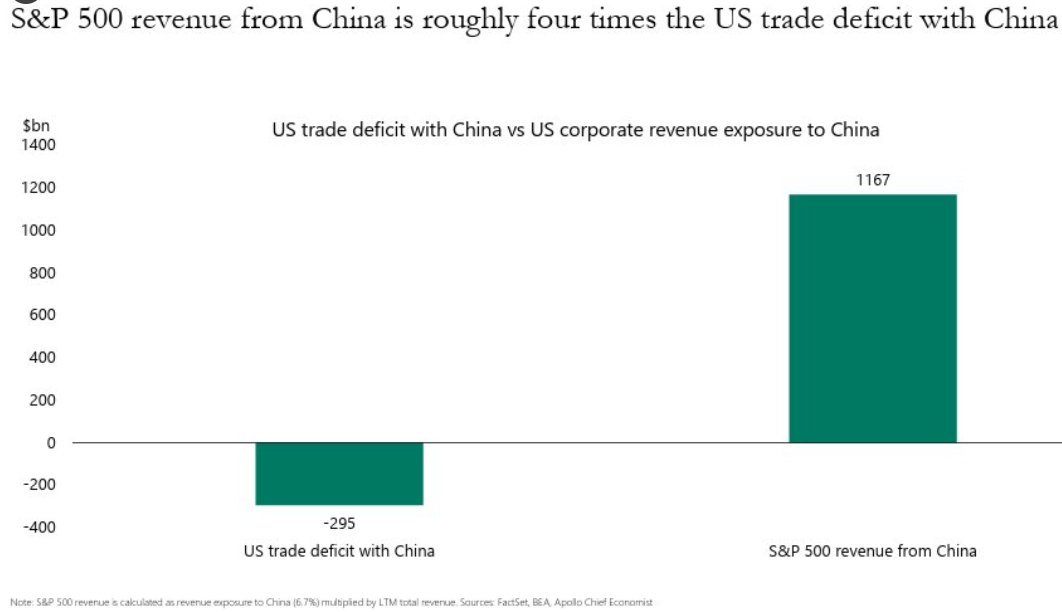

Apollo’s Torsten Sløk: “US companies made $1.2 trillion in revenue selling to Chinese consumers…The bottom line is that if the US has to decouple completely from China, it would result in a significant decline in earnings for S&P 500 companies…” (Chart 1, Apollo)

Google down 8% while Nvidia surges as President Trump prepares to remove Biden-era chip export restrictions.

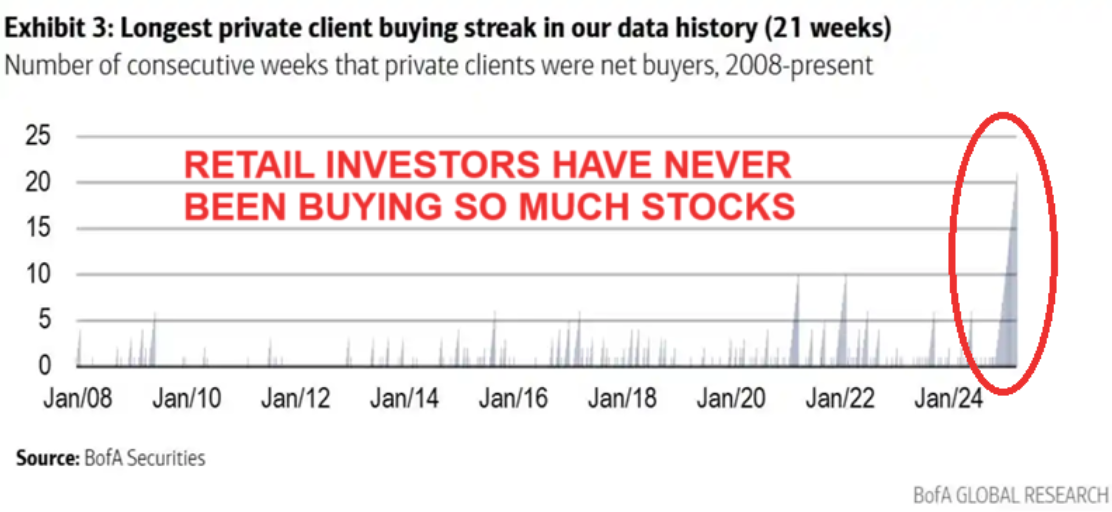

Same story but this time different author…. This has NEVER happened before: Retail investors have been buying US equities for 21 weeks STRAIGHT, the longest streak EVER. This significantly beats the previous record of 10 consecutive weeks before the 2022 BEAR MARKET. All while hedge funds have dumped more than ever. (Chart 2, BofA Global Research)

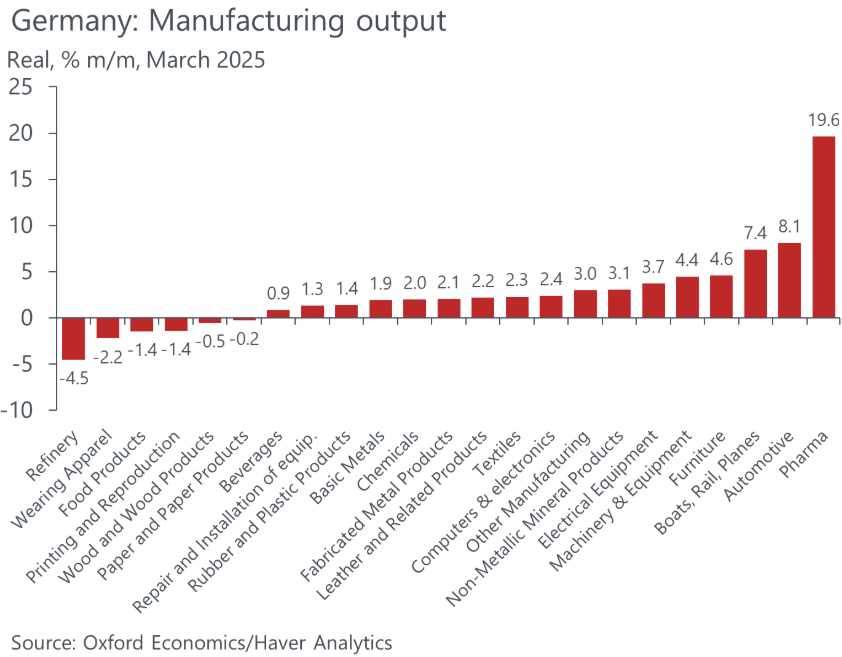

Big surge in German IP in March. The 20% surge in pharma was likely due to US tariff front-running. But gains were broad-based. Easter in April may be another reason. Surveys/orders speak against this surge lasting. (Chart 3, Oxford Economics, Haver Analytics)

Data today – Bank of England policy meeting (25bp cut expected and fully priced in the OIS market). US initial claims and continuing claims.

Morning Macro 7th May

Overnight risk assets rallied and safe haven assets dropped on two sets of positive news. More stimulus from China’s central bank and an announcement that China & US will hold talks in Switzerland at the highest possible level (outside of the Presidents).

China’s Vice Premier He Lifeng to meet US Treasury Secretary Bessent – Chinese Ministry of Foreign Affairs.

China to cut a series of rates: Reserve ratio requirement by 0.5ppt 7-day reverse repo to 1.4% (from 1.5%) Structural tools rate by 0.25 ppt.

India strikes Pakistan. Pakistan says it shot down Indian planes, taken some prisoners.

FX intervention sends HKD rates down most in 17 years.

According to Paul Tudor Jones even if Trump slashes China tariffs by 50%, the stock market is still on track to make new lows.

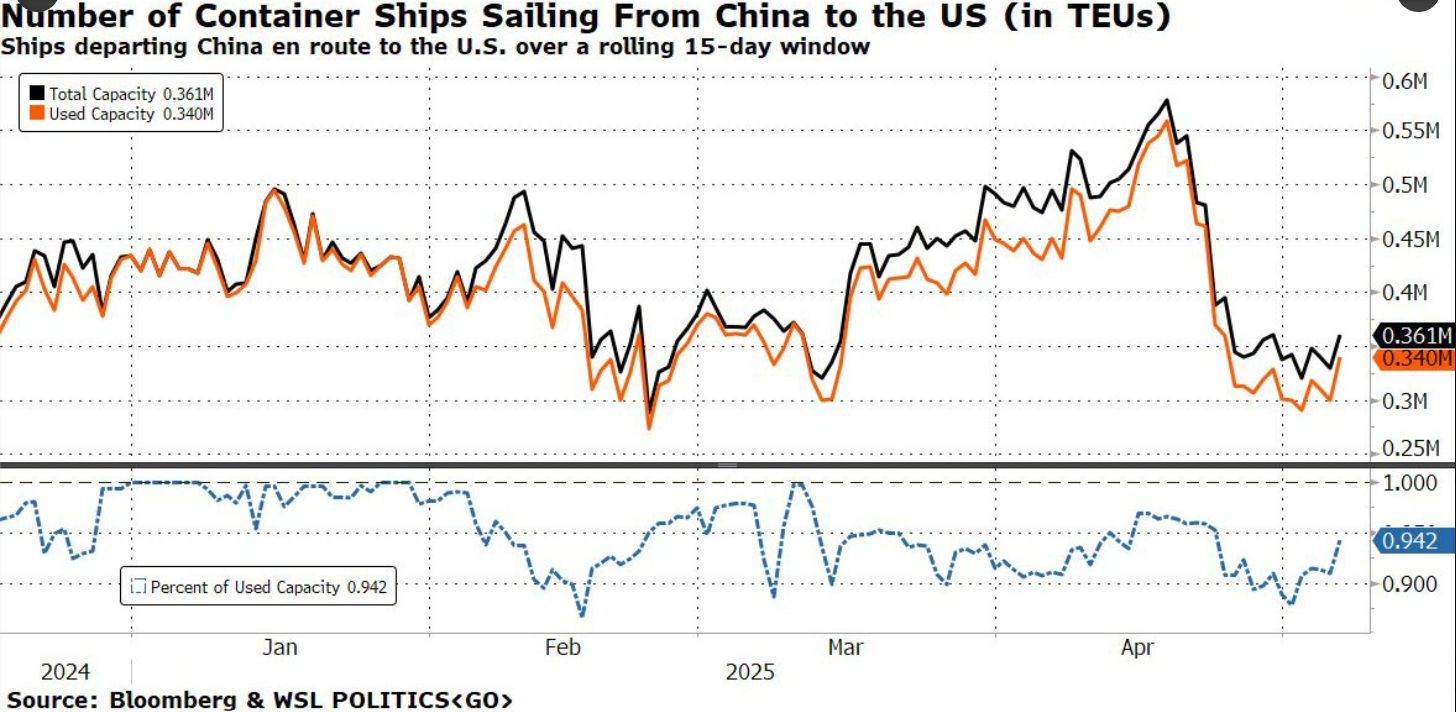

Container shipments on route to the US from China hit a 2-week high.(Chart 1, Bloomberg & WSL politics)

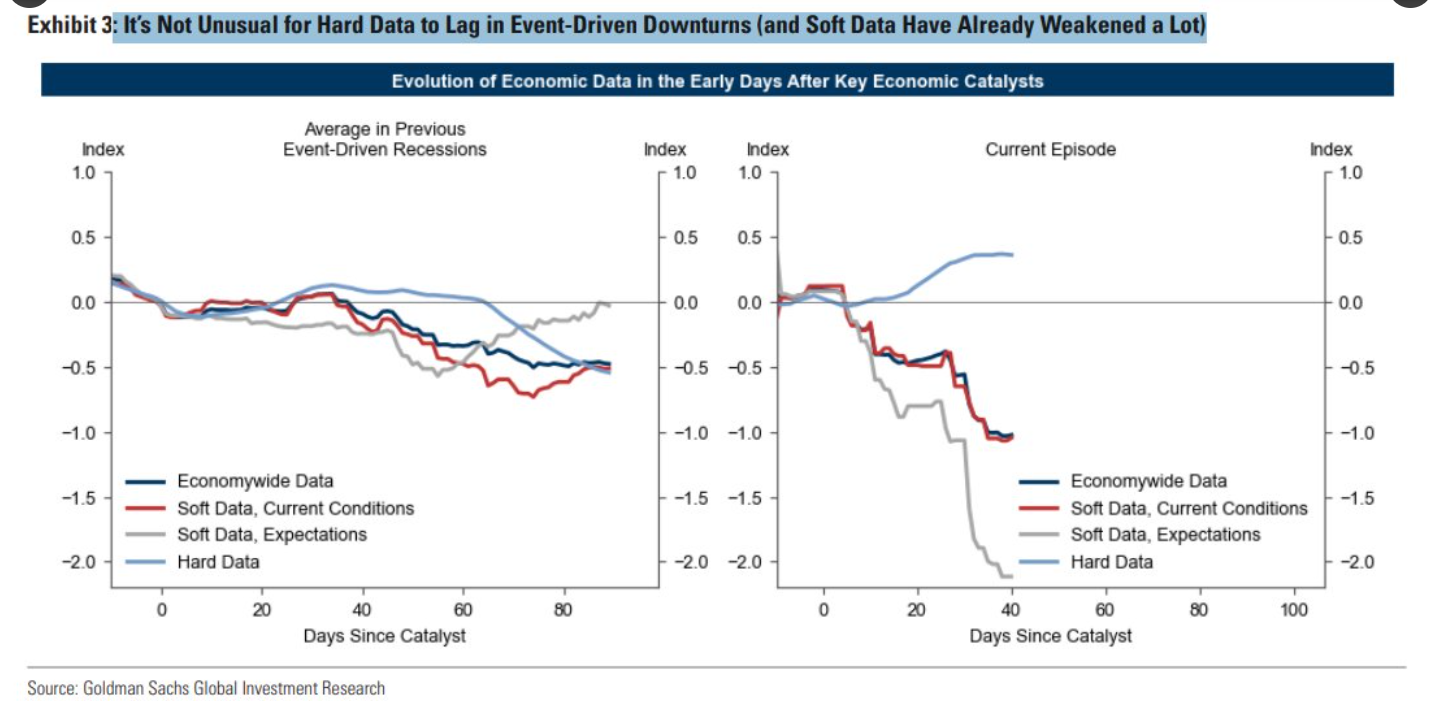

GS: It’s Not Unusual for Hard Data to Lag in Event-Driven Downturns (and Soft Data Have Already Weakened a Lot) (Chart 2 , Goldman Sachs Investment Research)

TESLA’S CAR SALES IN UK FELL 62% YoY LAST MONTH TO THE LOWEST LEVEL IN OVER 2 YEARS

Data today – U.S. Fed FOMC interest rate policy meeting tonight. No change expected but watch the rhetoric over inflation and the tariff impact on growth, a strain on either side of their inflation/growth dual mandate. The overnight index swap prices 8bp cuts at their next 18th June meeting and a total of 106 bp cuts over the next 12 months.

Morning Macro 6th May

Gold surges again, +4.1% in 2 days and the dollar weakens especially against Asian currencies on frustration with the lack of positive tariff news.

Bessent: Tariffs, tax cuts and deregulation are keys to drive long-term investment

Asian currencies are struggling with dollar weakness, especially Tiawan, Hong Kong, South Korea & Singapore.

Hong Kong Ramps Up FX Intervention to Defend Currency Peg – Bloomberg

Taiwanese dollar surges for the second day. A 17 standard deviation move (Chart 1, Gavekal Research, Macrobond)

ISM Services Index came in stronger than expected, a surprise given the weakness in the regional Fed surveys. 52.3 vs 50.5 prior. But the prices paid component rose to 65.1 its highest level since January 2023.

Per TradeGov there were approximately 500k fewer air passenger arrivals into U.S. in March 2025 compared to same month last year as tourists shun the U.S. (Chart 2,International Trade Administration, Arbor data science)

Institutional investors have rarely been this BEARISH on US stocks: Hedge funds’ shorting of US-listed ETFs hit a RECORD high in April. This even surpassed the levels seen during the 2020 market CRASH. Meanwhile, retail investors bought the most equities in history.(Chart 3, Goldman Sachs)

Hard Brexit reduced worldwide UK exports by 6.4% & worldwide imports by 3.1%, Centre for Economic Performance at LSE.

Data today – EZ PPI

Morning Macro 2nd May

Risk rallied yesterday as economic data came in less weak than expected! Gold also sold off to $3,200 on hopes of positive tariff news. The main focus today will be U.S. non-farm payrolls at 8.30 EST, with market expecting a weak number (+130k, 4.2%) after poor regional surveys and weaker ADP & initial claims.

US ISM Manufacturing Mar: 48.7 (est 47.9; prev 50.3) – Prices Paid: 69.8 (est 73.0; prev 69.4) – New Orders: 47.2 (est 45.0; prev 48.6) – Employment: 46.5 (est 44.6; prev 47.6)

Initial jobless claims jump to 241k from 223k while continuing jobless claims jump to a new cycle high of 1.916M

March construction spending -0.5% month/month vs. +0.2% est. & +0.6% prior (rev down from +0.7%)

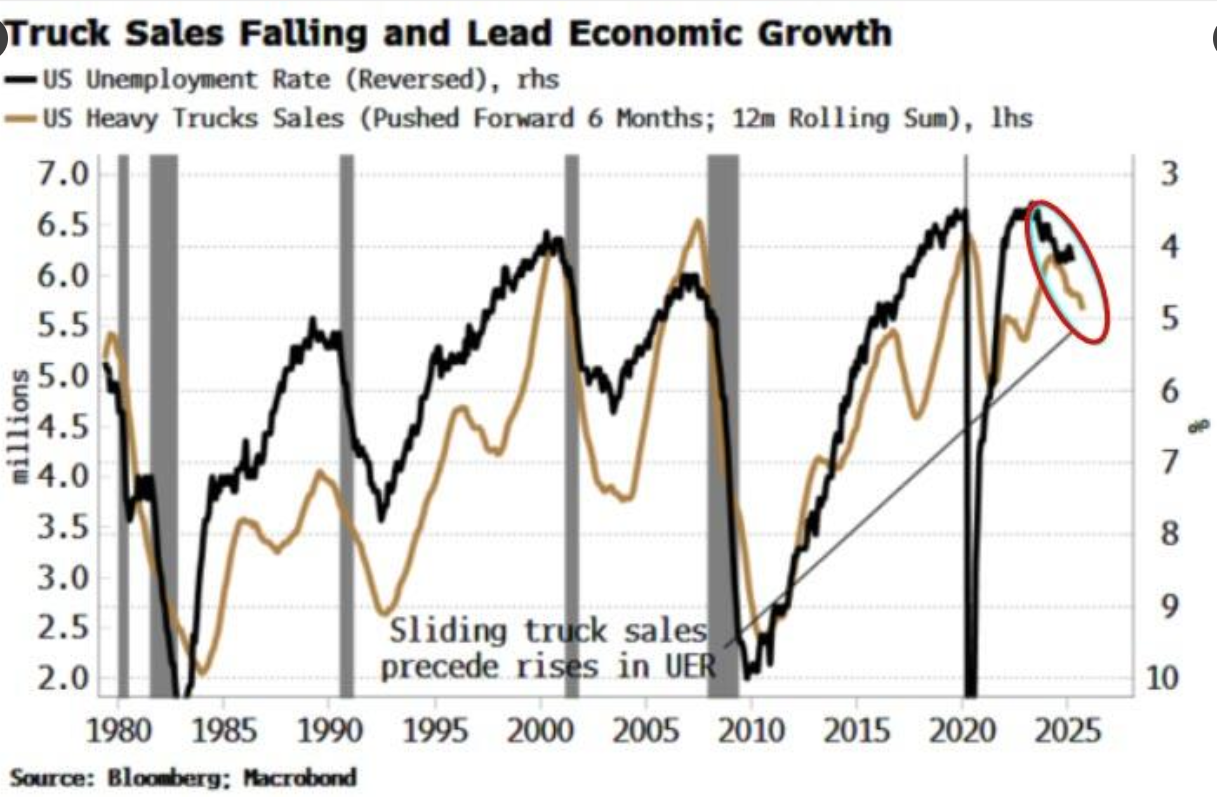

Truck sales trending nicely, but in the wrong direction (Chart 1, Bloomberg, Macrobond)

More pressure on Powell, this time from Tsy Sec Bessent…

Tariff headlines….

Trump: Whoever takes oil from Iran cannot do business with the US.

There is no fear of recession in the equity market. S&P 500 forward PE – Recession Periods

2025: 19.9x (current) vs.

2020: 13.4x

2002: 12.8x

1990: 10.1x

2008: 8.9x

1980: 6.5x

1982: 6.0x

What is remarkable about April’s U.S. equity trading, is that institutional investors dumped at the lows and stayed out, while retail kept buying the entire time.(Chart 2, Goldman Sachs, Bloomberg)

And (Chart 3, JP Morgan)

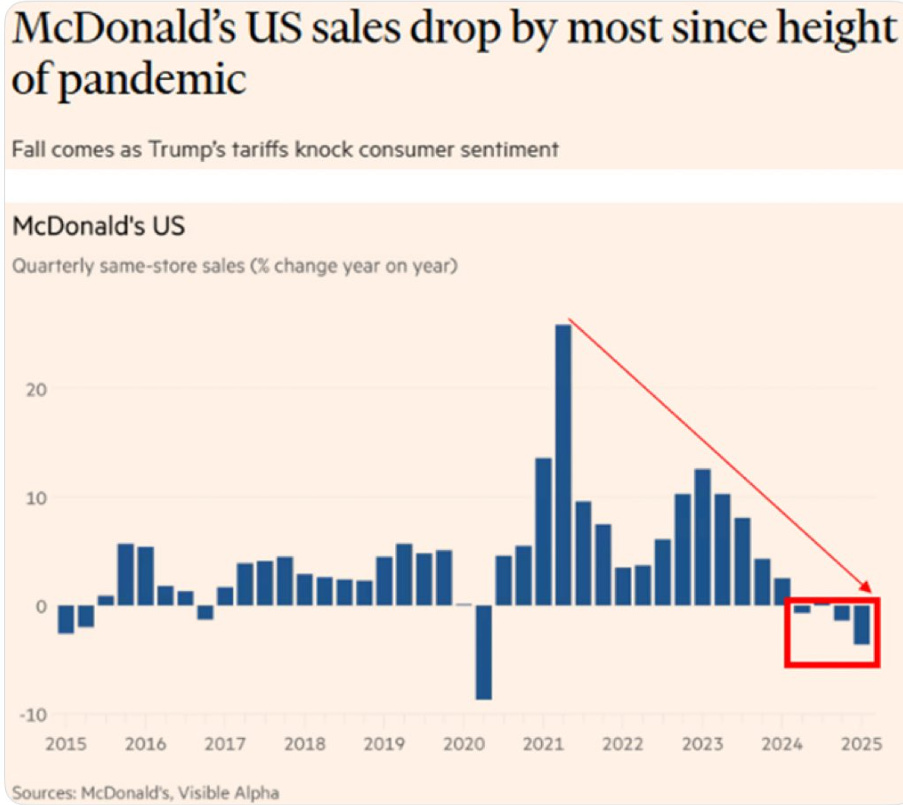

McDonalds sales fall most since covid (Chart 4, McDonalds, FT, Visible Alpha)

Data today – US payrolls (est +130k, with 4.2% unemployment rate)

Morning Macro 1st May

Weak data from the US sees the overnight index swap market price exactly 100 basis points of cuts from the Federal Reserve this year.

US GDP Annualized (Q/Q) Q1 A: -0.3% (est -0.2%; prev 2.4%) –

Personal Consumption: 1.8% (est 1.2%; prev 4.0%) –

GDP Price Index: 3.7% (est 3.1%; prev 2.3%) –

Core PCE Price Index (Q/Q): 3.5% (est 3.1%; prev 2.6%) –

Employment Cost Index: 0.9% (est 0.9%; prev 0.9%

ADP US APRIL PRIVATE EMPLOYMENT: 62,000; EST. +114K – Lower than every Bloomberg economist estimates…. a bad lead into US payrolls employment data on Friday.

Also a negative GDP print from Canada…. Canada GDP for February -0.2% versus 0.0% estimate

More jaw-boning from the Trump administration, but this is ridiculous… “On today’s news, that’s the best negative print I have ever seen in my life”. – Peter Navarro

Plus Donald Trump – This is Biden’s stock market, not Trump’s.

BOJ unchanged as expected but Yen weakens on comment…..

BOJ governor Ueda: Underlying inflation to cool down due to tariffs, slower global growth.

BOJ governor Ueda: Uncertainty stemming from trade policies have heightened sharply

Japan PM Ishiba: Our basic stance that we request abolition of US tariffs has not changed.

Another negative German GDP print, the longest recession since unification. (Chart 1, Bloomberg)

Conference Board’s labour differential (jobs plentiful – jobs hard to get, blue) fell in April, and overall trend continues to suggest upward pressure for unemployment rate (orange) Key data today – US ISM manufacturing (Chart 2, Bloomberg, @LizAnnSonders)

Key data today – US ISM Manufacturing PMI (est 48, last 49)…… but risk of a very bad number, recent regional reports suggest significantly lower.

Morning Macro 30th April

A small bounce in risk overnight on Trumps bravado (we are going to make a deal with China) but then much weaker official PMI data out of China reversed sentiment. China’s 10-year bond yield is now back at its cycle lows 1.61%, and Brent is lower at $63.2. I cannot see how a U.S. recession can be avoided. Central banks need to cut more aggressively (inflation spikes are not demand led) and tariff agreements need to be made, or tariffs repealed, but unfortunately we have leaders who will not back down.

China’s Apr manufacturing PMI slumped into contraction at 49.00 (vs 50.50 in Mar)

Apr new export orders plunged to 44.7 in Apr, the lowest reading since Dec ’22. Non-Manufacturing PMI 50.4[Prev.50.8]

March JOLTS job openings down to 7.192M vs. 7.5M est. & 7.48M prior (rev down from 7.568M) (Chart 1, Bloomberg), a reminder that JOLTS lags other labour market data by a month. Also, the JOLTS quits rate moved up to 2.1% in March. All bad news.

Another poor consumer confidence number. Conference Board Consumer Confidence fell to 86.0, the lowest level since May 2020. Expectations (red line, bottom chart) fell to the lowest level since 2011.NY Empire state manufacturing 6M ahead orders just plunged to a record low. (Chart 2, Bloomberg)

Plus Year-ahead median inflation expectations continue to soar per the Conference board up to 6% in April (Chart 3, Bloomberg)

More tariff rhetoric….

Worth noting and not trying to draw comparisons between 2025 and 2008. No two crises are the same. But just as a historical lesson. Bear Stearns collapsed in March 2008. Stocks rallied essentially uninterrupted all spring and summer long. And were +15% higher by the end of August 2008. And then reality finally settled in.

Key data today – EZ CPI & GDP, US Q1 GDP, Employment cost index, PCE prices, ADP, Canadian GDP

Morning Macro 29th April

Tariff ‘Chaos’ Drags Key Texas Manufacturing Gauge to Worst Since 2020 – Bloomberg (Chart 1, Bloomberg)… this also implies Thursday’s US ISM manufacturing will com in way below consensus.

JAPAN ECONOMY MINISTER AKAZAWA: NO CHANGE TO OUR STANCE WE ARE DEMANDING FULL REMOVAL OF U.S. TARIFFS

“It normally takes 18 months on average for the US to negotiate a trade deal.” – Apollo’s Torsten Sløk

The rate of deficit spending is trending seasonably higher than any other year since the pandemic, per the Peter G Peterson Foundation. (Chart 2)

German GfK consumer confidence improves -20.6 vs -24.3 last

The soft data suggests that the hard data is set to fall. Consumer Confidence can lead the unemployment rate (inverted). If that ends up being the case this time around, we’re looking at around 6% or higher.(Chart 3 , Goldman Sachs)

Southwest Airlines CEO last week: “I don’t care if you call it a recession or not, in this industry, that’s a recession”

Today’s data – US consumer confidence, JOLTS data, house price index

Morning Macro 28th April

In the 3 weeks since the tariffs took effect, ocean container bookings from China to the United States are down over 60% industry wide. There are comparisons between the fall in container bookings from covid and current tariff dispute. But they are different, there will be disruptions for nonessential goods manufactured in Asia, but unlike during Covid, corporations will pay higher prices for critical components to avoid production halts at home. (Chart 1, Vizion, FT)

Four charts from Apollo highlighting the woes striking the U.S. economy. Manufacturing outlook has collapsed in U.S. (Chart 2, Source Apollo)

There’s also a sharp decline in US corporate capital expenditure plans (Chart 3, Source Apollo)

Cost pressures increasing based on Fed manufacturing survey (Chart 4, Source Apollo)

And consumer confidence now lower than in the GFC (Chart 5, Apollo)

While President Trump still tries to make it all sound so good…. When Tariffs cut in, many people’s Income Taxes will be substantially reduced, maybe even completely eliminated. Focus will be on people making less than $200,000 a year. Also, massive numbers of jobs are already being created, with new plants and factories currently being built or planned. It will be a BONANZA FOR AMERICA!!! THE EXTERNAL REVENUE SERVICE IS HAPPENING!!!

Shein hikes prices as much as 377% ahead of tariff increases.

And finally, a HUGE week of economic data where the tariff woes will start to show up more clearly –

Tuesday – US consumer confidence, JOLTS data, house price index

Wednesday – China PMI, EZ CPI & GDP, US Q1 GDP, PCE prices, ADP, Aussie CPI, Canadian GDP

Thursday – BOJ rate decision, US ISM manufacturing

Friday – US employment data

NOTE: 25% S&P500 companies report earnings

Morning Macro 25th April

Despite Trump saying US-Chinese officials had met, while the Chinese denied this risk rallied yesterday on the continued tariff de-escalation. Nasdaq rallied 2.7%, S&P 2%, the dollar index edges back towards the key 100 level, and gold drifts back below $3,300 level (having peaked at $3,500).

Overnight we also had more positive noises from China….

BREAKING: China is considering suspending its 125% tariffs on some U.S. goods.

Plus bullish headlines from China’s politburo….POLITBURO HOLDS MEETING: XINHUA – BBG

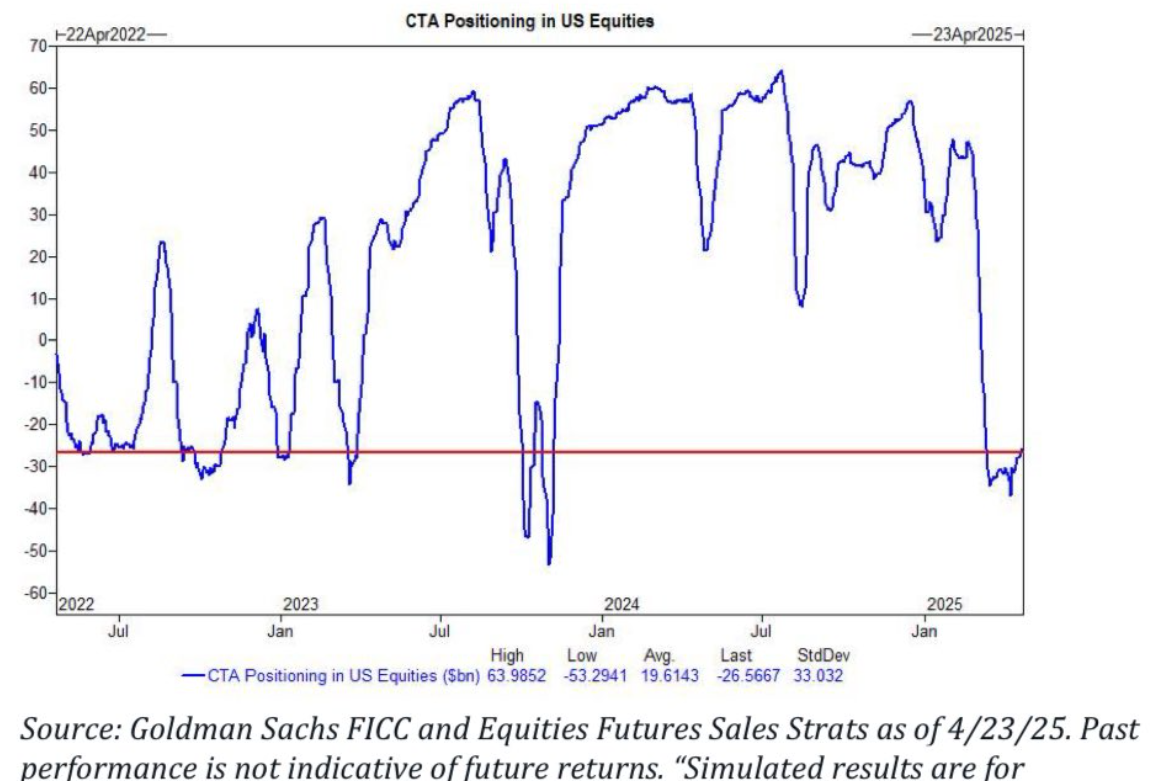

CTAs have now begun buying U.S. equities from a -$26B net short position.(Chart 1)

U.S. Existing home contract closings decreased 5.9% last month to an annualized rate of 4.02 million, the weakest March since 2009.

U.S. trucking volumes down 8.3% month over month… We are approaching COVID low levels in trucking. The market continues to stall. (Chart, Craig Fuller @freightalley)

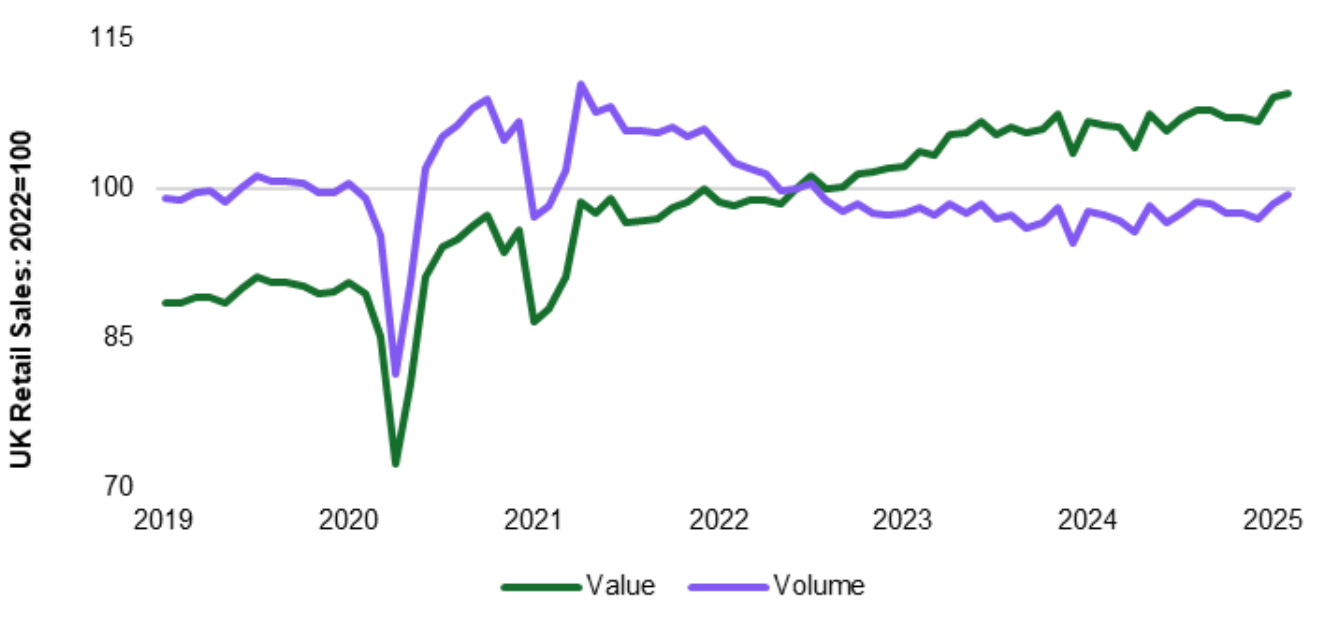

Mixed UK data. UK retail sales surprise to the upside. Retail sales volumes were up 0.4% in March 2025, following a rise of 0.7% in February 2025 (revised down from 1.0%).

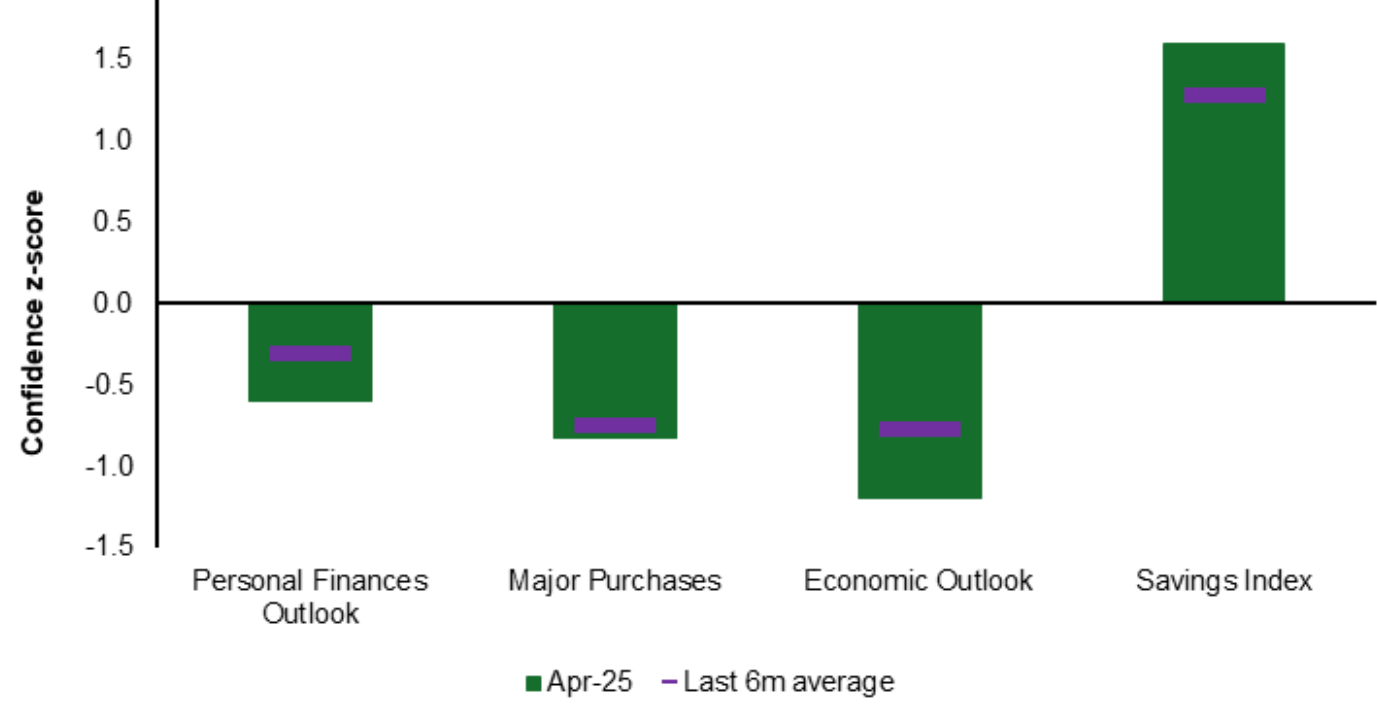

While UK consumer confidence came in weaker than expected. All three sub-indicators below their long term and 6m averages. Savings Index back up to near its all-time high, suggesting a more cautious spending start to Q2. (Chart 1, source @frencheconomics)

Japan Tokyo CPI. All inflation measures accelerated significantly in April 2025. Core CPI reached its highest level in two years (since April 2023). Market expectations for Core CPI were 3.2%, actual came in higher at 3.4%. BOJ expected to keep policy rate unchanged at 0.5% despite inflation uptick. Measure April MoM Chg Tokyo CPI +3.5% yoy, +0.6% mom. (Chart 2, @macro84)

APPLE PLANS TO SHIFT THE ASSEMBLY OF ALL US-SOLD IPHONES TO INDIA AS SOON AS NEXT YEAR – FT

Denmark’s Novo Nordisk continues its downtrend, now down 58%.

Data today – Canada retails sales, US Michigan consumer sentiment

Morning Macro 24th April

Risk rallied on the flurry of positive headlines from Washington (though the rally appears to be fading already this morning). Nasdaq rose yesterday 2.3%, S&P 1.7% and gold fell 7.7% from the highs. Though as I say the relief seems to be fading this morning with equities falling and gold bouncing again on the headline ….China ForMin Spox: China, US Not Yet In Talks On Tariffs; Will Fight Tariff War If We Must

Some of yesterday’s headlines

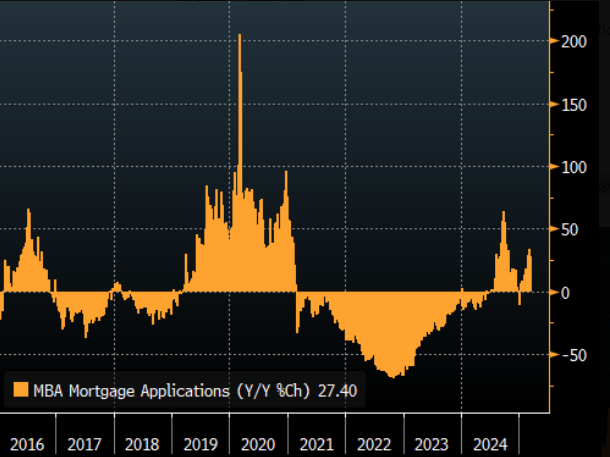

MBA mortgage applications fell -12.7% this past week vs. -8.5% prior…. the largest weekly decline since October

Flash PMIs came in weaker than expected across the board. Note these are diffusion indicators, above/below 50 is expansion/contraction.

6-month outlook for new orders (blue) and employment (orange) per Richmond Fed

Manufacturing Index both fell into contraction territory in April (Chart 1, Bloomberg)

Regarding the tariff we haven’t started to see the impact yet, but it’s coming. It takes 25 days for shipping containers to go from China to LA, and 35 days to New York.

Brent drops on reports several OPEC+ members want to accelerate return of barrels again from June

Lagarde Says Tariffs Likely More Disinflationary Than Inflationary…. (for Europe).

Bridgewater, the largest hedge fund in the world turns (very) bearish.(Chart 2)

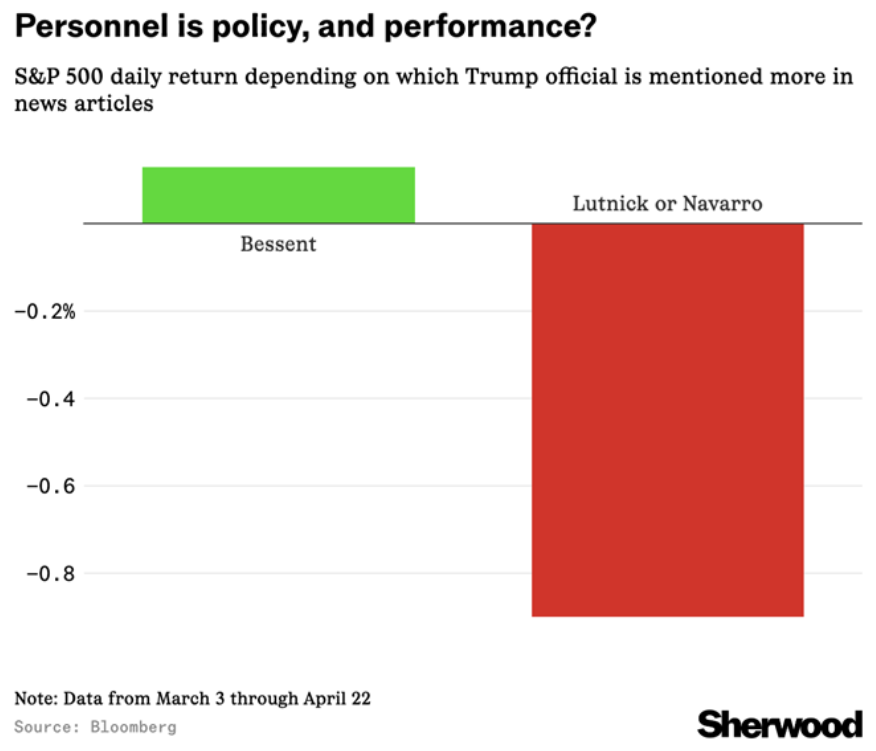

As we’ve said many times Tsy Sec Scott Bessent is the member of the Trump team with the credibility. (Chart 3)

Data today – French & German consumer confidence, US durable goods orders & existing home sales.

Morning Macro 23rd April

Trump backed down overnight on both China and Fed’s Jerome Powell, so equities are up in overnight trading (|Nasdaq +2%, S&P +1.7%), having rallied yesterday 2.5% (on Tsy Sec Bessent’s comments that the tariff standoff with China is unsustainable). The dollar has recovered 1.3% from the lows and gold is lower -5.3% from yesterday’s high. Relief can be seen elsewhere with the US 30-year bond 12bp lower, and the US yield curve 2s/10s also 12bp lower.

The market is also excited about Bessent’s presentation today on the State of the Financial System, 10am EST.

More jawboning from Trumps team to talk up the markets – US and India have finalized terms for a trade deal, says VP Vance.

April Philadelphia Fed Services Index dropped to -42.7 vs. -32.5 prior, lowest since 2020.

IMF cut Germany’s growth outlook to zero (Chart 1, IMF)

China as warned South Korean companies not to export products containing China’s rare earth minerals to the US military and defence firms, Korea Economic Daily reports, citing unidentified government and company sources.

Big miss on Tesla earnings

Chip giant Intel to lay off another 20,000 employees after laying off 35,000 employees just a few months ago to save money

Data today – EZ, UK & US PMIs, plus US mortgage application & new home sales

Morning Macro 17th April

Powell ditched the transitory prognosis yesterday, saying inflationary effects of tariffs may be more persistent. He noted the economic impact of tariffs is likely larger than expected and even suggested the Fed may find their mandates in tension. Sounds like stagflation is slowly becoming the base case. The Fed could quickly find themselves unable to cut as the labour market would like out of fear for higher inflation. Powell noted the Fed is well positioned to wait for more clarity for the time being. Back to higher for longer.

The OIS was little changed is currently pricing 85 bps of cuts throughout the rest of 2025, although the timing of the first cut is being extended, now pricing July compared to June on the 11th April.

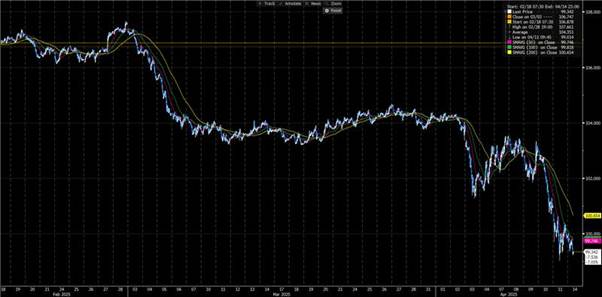

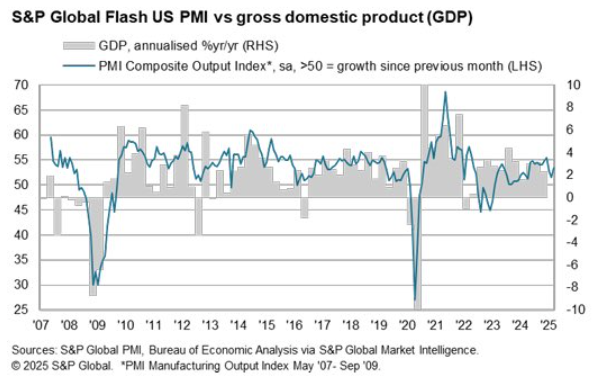

But US equities fell rapidly, with S&P 500 emini futures down 2.25% yesterday and Nasdaq eminis down 3% – led by Nvidia down 6.9% (figure 1). TSMC is sticking to its forecasts, despite tariffs – says still very strong demand, especially in US. Asian indices did well today: Nikkei 225 recovered 1.8% and Nifty 50 is up 1% too. While gold hit another ATH at $3357.92/oz!

US retail sales printed strong at 1.4% m/m growth in March, up from a sluggish 0.2% m/m growth in February and in line with consensus expectations (figure 2). This was the biggest increase in retail sales since January 2023, as households front load consumption ahead of tariffs. On a y/y basis retail sales surged up 4.6% from 3.5% in Feb. Can it last with consumer goods about to get expensive?

US industrial production was less positive, falling by 0.3% m/m in March, reversing some of the 0.8% increase in February. The manufacturing sector is only about 10% of US GDP, and Trump wants this to be higher. The data is going in the wrong direction.

Today we get the ECB interest rate decision where markets are expecting a full cut, OIS pricing 24.5 bps of cuts.

Data today: ECB decision, US housing data

Morning Macro 16th April

White House – “China now faces up to a 245% tariff on imports to the United States as a result of its retaliatory actions”. Just call it an embargo…

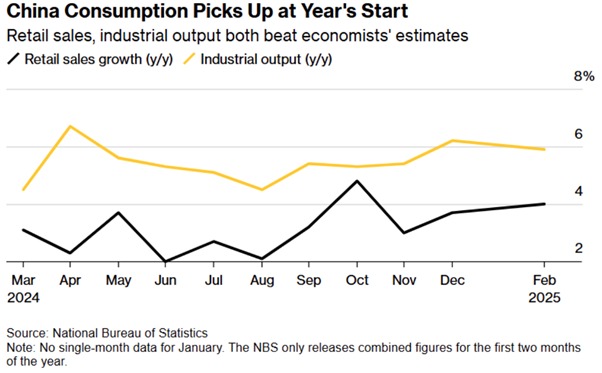

Chinese data surprisingly strong. According to the National Bureau of Statistics, China grew by 5.4% y/y in Q1, ahead of consensus of 5.2% and much higher than UBS forecast for 2025 growth of 3.4%. QoQ, China grew by 1.2%. March retail sales were strong, accelerating to 5.9% y/y and far above consensus estimates of 4.2%. Retail sales posted the strongest growth since December 2023. Industrial output also outperformed expectations, printing 7.7% growth y/y, ahead of expectations of 5.9%. YTD fixed asset investment rose 4.2%, up from 4.1% from the previous month.

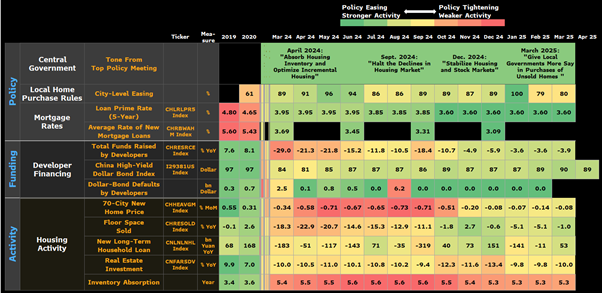

Less reassuring is the YTD property development investment which fell by 9.9% y/y, in line with consensus, but worse than the 9.8% decline for the period Jan/Feb. But China house prices are down 4.5% y/y, slowing marginally from -4.8% in Feb. Across a broad set of indicators the housing market does show signs of stabilization (Figure 1). The health of the property sector in China remains a key focus for policy and drives consumer confidence.

Even despite the big upside surprise among core macro prints in China, equities were more focused on the potential for tariffs to be raised further to 245%. Led by the Hang Seng’s decline of -2.53%, onshore bourses were down with CSI 300 -0.93%, Shanghai -0.92% and Shenzhen -2.25%, respectively. CGB 10-year yields fell 2 bps – not a sign of confidence.

Another all time high for gold at over $3,297/oz (Figure 2). Amidst safe haven flow, Gold got a boost from weak gold production. According to Statistics South Africa, gold production fell 7.6% y/y in February, down from +1% in Jan.

Trade war spirals: the Trump administration has banned Nvidia from selling its H20 chip to China, escalating the tech conflict with Beijing, expected to cost the company $5.5bn, despite the chip being designed to meet earlier US restrictions. Nvidia stock fell 6% after hours.

Data today: US retail sales, industrial production, mortgage applications.

Morning Macro 15th April

Trump on Monday hinted at possible exemptions to existing auto-related tariffs. This follows exemptions granted to certain electronics over the weekend.

According to the New York Fed, year-ahead consumer inflation expectations rose 0.45% to 3.58% in March, the highest since September 2023. Three-year expectations held at 3.00%, while five-year expectations edged down to 2.86%. Atlanta Fed President Raphael Bostic said Monday the Fed is in a “pause position,” awaiting more economic clarity, echoing business sentiment. OIS has retraced, now pricing in 83 bps of cuts by year-end, down from 102 bps on April 8, as markets begin to normalize.

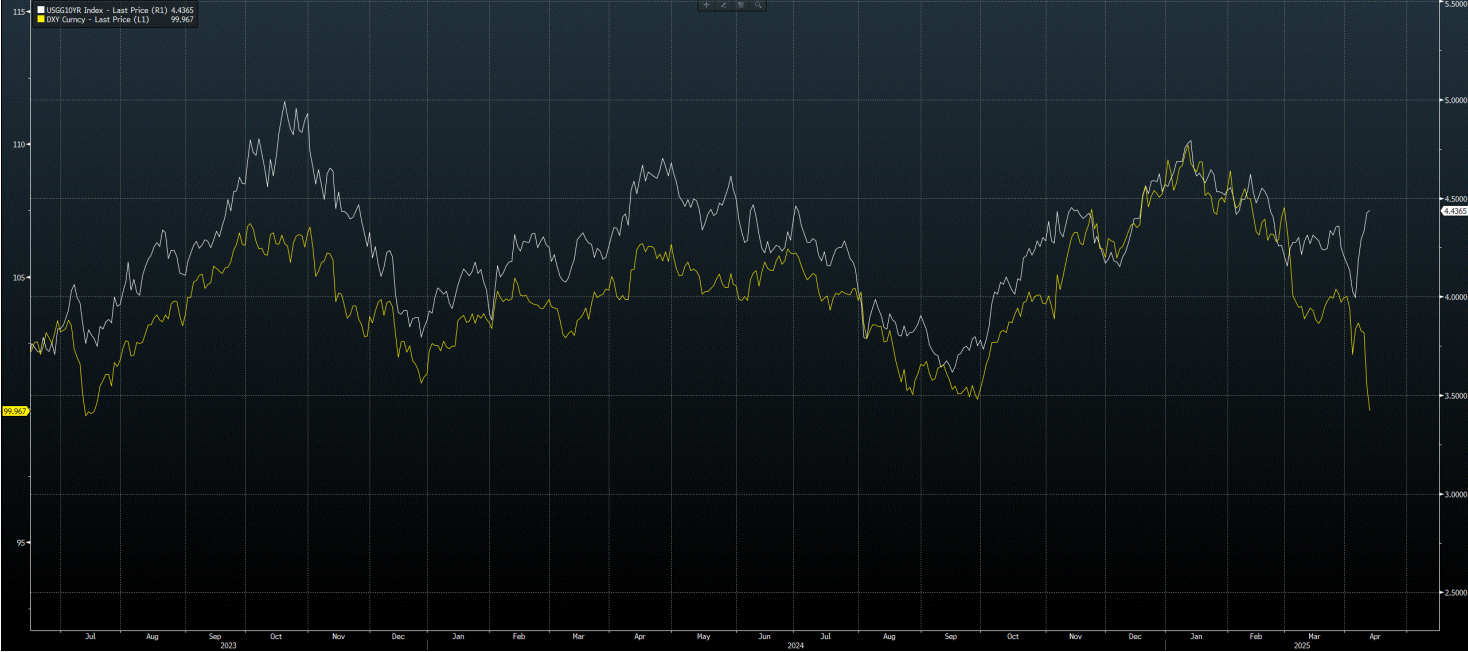

The 10 year yield (Chart 1) has retraced a little to 4.34% down from a high of 4.59% last week, as Bessent downplays the recent bond market selloff, and highlighting that the Treasury has tools for addressing dislocation if and when needed. The aggressive dollar selling, which saw the yield-dollar correlation breakdown, seems to have started to slow too, with the DXY trading in a tight range this morning around 99.7.

Consumer prices are printing hotter in NZ, with food prices climbing 3.5% y/y in March, up from 2.4% in February. Stats NZ attributed the increase primarily to higher prices in the grocery food and meat, poultry, and fish categories, which rose 5.1% and 5.3%. NZD is tearing higher (chart 2) against USD making new YTD highs.

India’s wholesale prices increased by less than expected in March, up by 2.05% y/y compared with 2.5% expected. Within the breakdown, primary articles rose 0.76%; fuel, power and lighting prices rose 0.2%; manufactured product prices increased by 3.07%; and wholesale food prices were up 1.57%.

Data today: Euro Area Industrial Production, ZEW Economic sentiment

Morning Macro 14 April

After initial reprieve on Friday, Trump once again pledged tariffs on electronics will go ahead. “NOBODY is getting off the hook”. These key consumer goods are not getting exemptions, “just moving to a different Tariff ‘bucket’”.

Stocks benefited from the tariff delay this morning, despite Trump’s comments on Sunday. Asian markets saw strong gains today. Hong Kong’s Hang Seng led, jumping 2.4%, with mainland indices also higher — CSI 300 0.47%, Shanghai 0.86%, and Shenzhen 1.5%. South Korea’s Kospi rose 0.91%. India’s NIFTY 50 rallied 1.9% ahead of this week’s CPI release, expected to soften further. Eurostoxx 600 gained 1.7%, SP500 emini futures up 1%, Nasdaq emini up 1.5%.

The DXY continued to sell off this morning, falling back to 99.301. EUR/USD continues to be bid, now around 1.1411. US treasury selling has abated somewhat. 10 year treasury yields trading at 4.456% after peaking at 4.59% on Friday.

China total new yuan loan growth increased 7.4% y/y in March up from 7.3% in Feb, the first month to accelerate since March 2023. Consumer confidence has weighed on credit growth in China, but the swathe of stimulus is starting to pass through.

China continued to fix yuan weaker against USD this morning, at 7.211, up from 7.2087 on Friday. Yuan now trading at the bottom of its 2% range this morning at 7.319 against the dollar. This will help exports – which are still strong!

China’s exports jumped 12.4% y/y in March to USD 313.91 billion, well above 4.4% expected. Exports surged 46% m/m — second-highest on record, trailing only the 47.5% spike in March 2023.

Yields on super-long Japanese Government Bonds (JGBs) are jumping ahead of a 20-year auction on Tuesday and rumours of a supplementary budget. The yield on the 30 year JGB jumped 16.3 bps this morning. BoJ Governor Kazou Ueda reiterates he won’t have any preconceptions over monetary policy.

USD/JPY came under pressure from the open, sliding to last week’s lows around 142. Unwinding of positions on Friday appears to have reversed. Critical support sits near 140. Spec interest in yen rising markedly, funds are getting longer.

Data this week: ECB interest rate decision, US retail sales, US Industrial Production, India inflation, EA industrial production, China GDP, China Industrial Production, China Retail Sales, US building Permits, Japanese Inflation.

Morning Macro 11th April

Despite the tariff postponement the bond market is cratering again. The 30 yr is up 18bp since Wednesday’s close to 4.95, gold has surged to $3,220 overnight and the dollar index has fallen below 100. (Yields higher and currency lower highlights market disdain, remember Liz Truss). Nasdaq closed yesterday down 4.5% and S&P down 3.4%, and futures are getting aggressively hit in Asia.

The irony that bond yields are rising sharply as we get the softest US inflation report in 4-5 years.

U.S. Mar. CPI (MoM): -0.1%, [Est. 0.1%, Prev. 0.2%]

U.S. Mar. CPI (YoY): 2.4%, [Est. 2.6%, Prev. 2.8%]

U.S. Mar. Core CPI (YoY): 2.8%, [Est. 3.0%, Prev. 3.1%]

My new favourite chart shows the breakdown in the correlation between the US 10-year yield (white) and the dollar index (yellow), breaking below 100. (Chart 1, Bloomberg).

Yesterday’s EUR/USD move was the largest in in at least 4 years. EUR is becoming a safe haven! The chart (Chart 2, Bloomberg) shows it clearly breaking a long-term resistance line, and it also show how much further it can go.

Other headlines that hit the wires across the day…..

EU AND CHINA START NEGOTIATIONS TO ABOLISH EU TARIFFS ON CHINESE ELECTRIC VEHICLES – HANDELSBLATT…As the US ramps up tariffs on China, the EU is attempting to reduce tariffs on China in an effort to build trade relations.

EU puts counter-tariffs on hold for 90 days after US pauses higher import taxes – follow the latest.

*EU, UAE AGREE TO LAUNCH FREE TRADE NEGOTIATIONS.

“I hope what they really do is let Scott Bessent negotiate… If you want to calm down the markets, show progress in trade deals and let Bessent negotiate.” – Jamie Dimon in his FOX interview…… BESSENT, ASKED ABOUT MARKET CONDITIONS: I DON’T SEE ANYTHING UNUSUAL TODAY

US President Trump recognises “transition difficulty” from tariffs as US markets drop again

*TRUMP SAYS HE HAVEN’T SEEN TODAY’S STOCK MARKET DROP (Chart 3)

US Steel Falls 10% After Trump Says He Doesn’t Want Japan Owner

BREAKING: TRUMP ADMINISTRATION IS CONSIDERING DELISTING CHINESE STOCKS ON U.S. EXCHANGES PER FOX NEWS

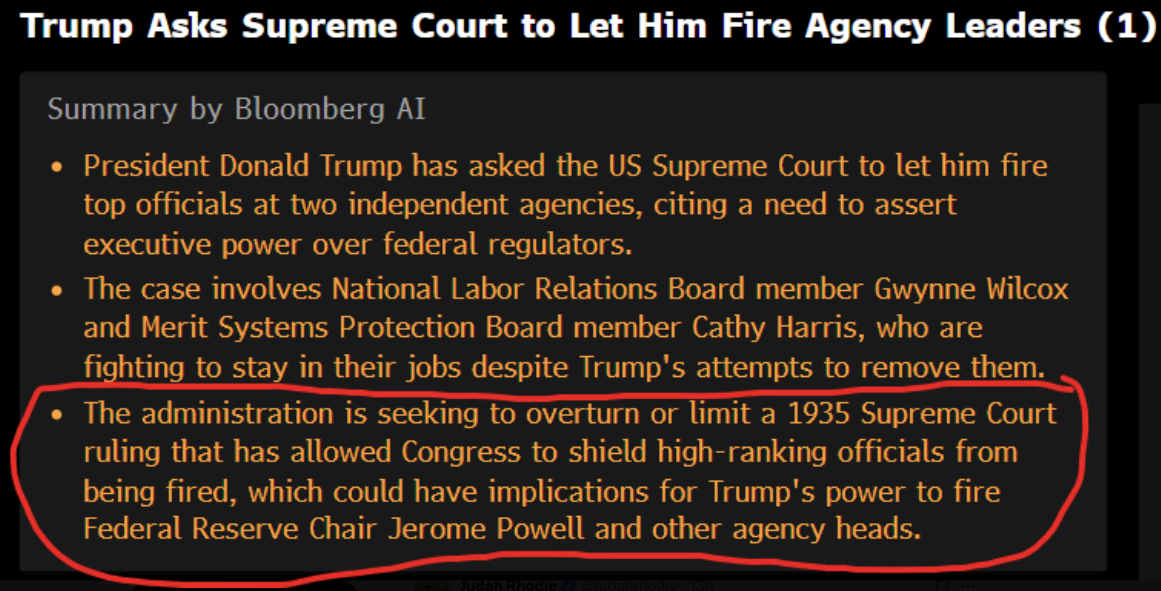

BREAKING: PRESIDENT TRUMP JUST ASKED THE SUPREME COURT FOR THE AUTHORITY TO FIRE FEDERAL RESERVE CHAIR JEROME POWELL Source BBG (Chart 4, Bloomberg)

Data today – U.S. PPI & Michigan consumer sentiment index.

Morning Macro 10th April

Trump blinked first (not China, and not the Fed), and the bond market broke his resolve with 30yr yields at 5% and the basis trade breaking Wall Street. Apparently, it was Bessent (multi decade fund manager) who explained the ramifications of the bond move to him. Trumps team still claimed it as a win as equities surged all the way back to last Friday’s levels. Nasdaq had its 2nd best day ever +12%, S&P500 had its 3rd best day ever +9.5%, but the biggest relief will be bond yields retreating (30yr fell from 5.02% to 4.73%).

Even so trade has collapsed with China and the remaining 10% tariffs will impact inflation. This is not a time companies will be investing, so data in the coming weeks will not be positive. Weaker growth and higher inflation in the U.S., while overnight data shows China remains in deflation, and Goldmans cuts it China growth outlook again from 4.5% to 4% for this year. The economic outlook remains bleak.

Trump lifted the tariff on China to 125% with immediate effect, announced a 90-day pause & cut reciprocal tariffs to 10% for nations that asked for talks. China imposes 84% retaliatory tariffs on U.S. goods. The 90-day ‘pause’ on tariffs does not apply to tariffs on Canada and Mexico. No change to autos, steel, and aluminium tariffs.

CHINA LEADERS TO MEET ON STIMULUS AFTER TRUMP’S TARIFF SHOCK

It’s also worth noting NASDAQ call volume spiked minutes before the 90-day tariff pause was announced. Not a good look for the White House.

In other news…..

China remains in deflation (Chart 1, Bloomberg):

*CHINA MARCH CONSUMER PRICES FALL -0.1% Y/Y; EST. 0%

*CHINA MARCH PRODUCER PRICES FALL -2.5% Y/Y; EST. -2.3%

Goldman Sachs cuts growth forecasts for China this year to 4.0% (from 4.5%)

The Chinese yuan weakened to levels last seen in 2007 today (Chart 2, Bloomberg)

Data today – US CPI (last 3.1%, estimate 3.0%), & weekly jobless claims.

Morning Macro 9th April

Carnage overnight in the bond market (which is 3x larger than the equity market). Since Friday’s close to now … the 30-year yield is up 56 bps, in three trading days. The last time this yield rose this much in 3 days (close to close) was January 7, 1982, when the yield was 14%. This kind of historic move is caused by a forced liquidation, not human managers make decisions about the outlook for rates. So while yields would typically fall during risk off emergencies these bond yields are actually rising, and sharply. The break down of the basis trade (correlation between bond yields and swap yields) will also cause staggering loses as these correlations are (usually) so tight and stable funds run huge positions (think LTCM 1998).

Amongst the headlines, overnight the Chinese currency fell hard (devaluation?), gold is finally bouncing, the U.S. 2’s10s yield curve has steepened sharply, the S&P fell 1.6%, Nasdaq fell 2% and Bitcoin sits on a key support line $76,600.

Japan’s MoF, BoJ, FSA hold an emergency meeting after…….. JAPAN’S 40-YR YIELD RISES 32BPS IN LESS THAN AN HOUR, TO HIGHEST SINCE DEBUT IN 2007

US President Trump’s reciprocal tariffs alongside the 104% levy on China came into effect

*CANADA SAYS IT’S ALREADY ANNOUNCED 25% COUNTER-TARIFFS AGAINST SOME U.S.-MADE AUTOS, WILL GO INTO EFFECT APRIL 9 *CANADA SAYS THE TARIFFS WILL REMAIN IN PLACE UNTIL U.S. ELIMINATES ITS TARIFFS AGAINST THE CANADIAN AUTO SECTOR

CHINA’S TOP LEADERS TO HOLD A MEETING AS SOON AS WEDNESDAY TO DISCUSS MEASURES TO BOOST ECONOMY AND STABILISE CAPITAL MARKETS AFTER US TRADE TARIFFS, SAY SOURCES…… Hang Seng Index jumps 2%.

Trump announces record-breaking $1 trillion Pentagon budget…… where’s DOGE?

RBI and RBNZ both cut their respective rates by 25bps as expected

ECB’s Nagel: Global growth prospects have deteriorated massively

Data today – US mortgage applications and FED minutes.

Morning Macro 8th April

The big news yesterday was not so much the fake news Tariff delay that temporarily sent risk surging, or even Trumps threat of an additional 50% tariff on China, but that swap spreads have surged to their widest ever levels. Swap spreads are the spread between the US bond yield and the interest rate swap yield. Both interest rate products but while one is the government sovereign debt the other is an interest rate derivative that fixes against the SOFR (Secured Overnight Funding Rate), Chart 1 is the historical spread between the two 30-year products, yesterday surging to a new all-time high. Investors are not only shunning US bonds but yesterday aggressively selling too.

Another way of looking at this is while equities stabilised yesterday, bond yields surged higher as investors sold them aggressively throughout the day (Chart 2, S&P500 vs 10-year US bond yield). While the S+P closed down just 0.2% on the day, the US 10-year yield surged 33 basis points from the lows. So, while equities look to have stabilised the credit markets are flashing increasing warning signals, and Treasury Secretary Bessent wish for lower yields for debt maturities is looking increasingly worrisome, with long end yields now higher than before the tariffs.

Not key data today!

Morning Macro 7th April

U.S. equity futures markets look to open down, Nasdaq -5.5%, S&P500 – 4.4% (15 min circuit breakers come in at -7%, -13% and market closes for the day at -20%). 2 year yields are down today -17bp as panic selling rips across Asia…..

Chinese stocks post biggest single-day loss since Global Financial Crisis

CHINA’S BEIJING STOCK EXCHANGE 50 INDEX TUMBLES MORE THAN 20%

BREAKING: CHINESE GOVERNMENT HAS STARTED CONDUCTING “STOCK MARKET STABILIZING OPERATIONS” AS THE CHINESE STOCK MARKET CONTINUES TO CRASH.

CHINA SOVEREIGN FUND SAYS TO FURTHER INCREASE ETF HOLDINGS

….. they’re not backing down on their tariff increases.

BREAKING: TRADING IS JAPANESE STOCK MARKET FUTURES HAVE JUST BEEN SUSPENDED AFTER HITTING CIRCUIT BREAKERS

THE EUROPEAN UNION AGREES ON A FIRST SET OF COUNTER MEASURE TARGETING $28 BILLION WORTH OF U.S. IMPORTS

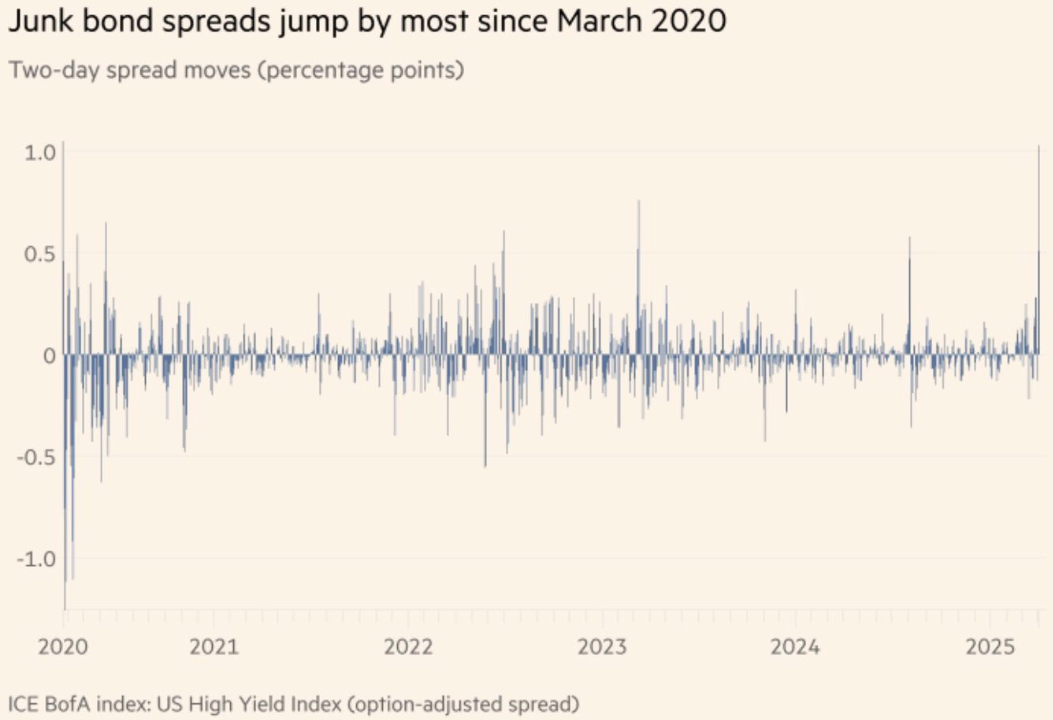

U.S junk bond spread rip higher (Chart 1, ICE BofA index). There will be staggering hedge fund losses announced soon, while retail traders are still buying!!! (see below)

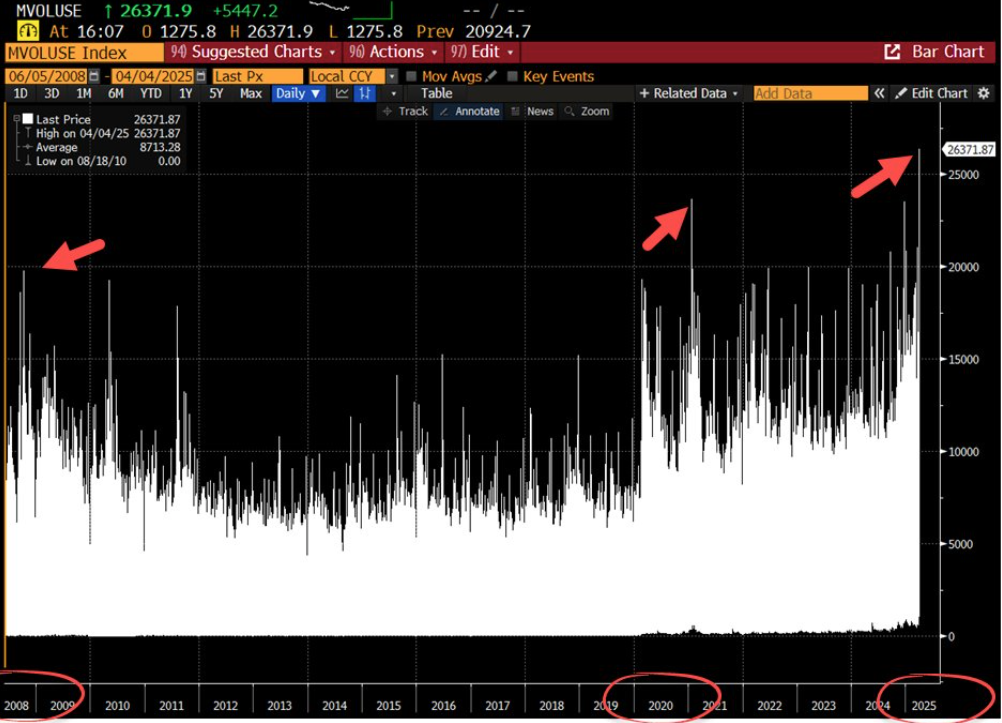

U.S. Equities Friday was the HIGHEST Volume (read: outright panic selling) trading day of ALL-TIME! (Chart 2, Bloomberg) while hedge funds sold the most volume of global stocks in 1 day since 2010 per Goldman Sachs on the other hand retail investors bought stocks worth $4.7 billion yesterday the largest amount in over 10 years per JP Morgan. Also Retail investors’ net inflows into US ETFs and single stocks hit a record ~$40 billion in March. This is ~$10 billion higher than the previous all-time high posted at the beginning of the 2022 bear market. Per JP Morgan.

German industrial production fell by 1.3% in Feb, a steeper decline than expected.

German Public-Sector Workers Win 5.8% Staggered Wage Increase.

Bitcoin down -10.5% since Friday’s close. ETHEREUM FALLS 10%, HITTING A NEW LOW SINCE MARCH 2023.

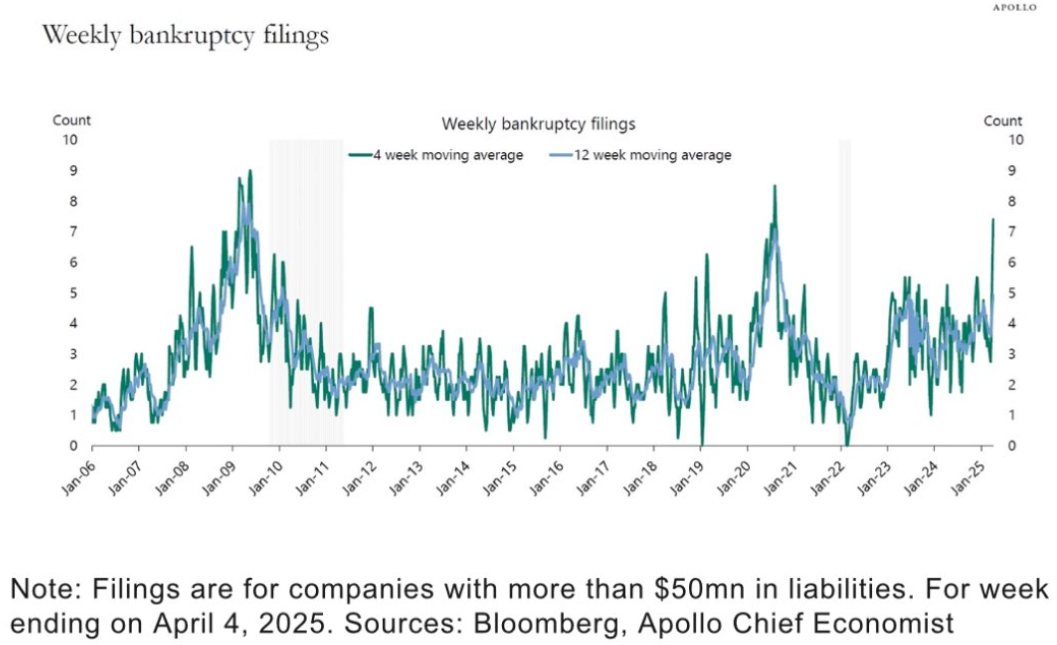

US corporate bankruptcies surging, even before the tariff announcements (Chart 3, Apollo).

Data this week

Tuesday – Australian consumer & business confidence

Wednesday – US mortgage applications

Thursday – US CPI, Chinese inflation

Friday – US PPI & Michigan consumer sentiment, UK ind prod

Morning Macro 4th April

More weak U.S. data but it was all about the reaction to Trumps tariffs. S&P500 -4.8%, Nasdaq Composite -5.9%, Dow Jones -9%, Gold another new high, albeit volatile), EURUSD rises 2% (biggest move since 2015), U.S. 2-year -15bp with the OIS now pricing 32% chance of a Fed cut in May (100% Fed cut in June). To add to the mix, we have U.S. employment data at 1.30pm today (135k expected with unemployment rate at 4.1%). Buckle up!

March ISM services 50.8 vs 53.0 expected — lowest since the pandemic (Chart 1, Bloomberg).

ISM Services employment surprises with a sharp turn lower this month. This is the 4th largest MoM decrease on record

U.S. CHALLENGER JOB CUTS (MAR) ACTUAL: 275.24K VS 172.017K PREVIOUS (Chart 2, Macrobond & Nordea)

U.S CHALLENGER JOB CUTS (YOY) ACTUAL: 204.8% VS 103.2% PREVIOUS

US CHALLENGER MARCH JOB CUTS JUMP TO HIGHEST SINCE MAY 2020

Great day for US growth? First tariffs and then lay-offs spreading outside of the government/DOGE…

The weakness in the dollar is counter-intuitive since usually the currency of tariff imposing country rises. Seems investors are more focused on potential weakness in US growth as a result of tariffs. It’s a substantial regressive tax – about 2% of GDP.

Germany February industrial orders 0.0% vs +3.5% m/m expected

Crude down over $6/bbl over the past 2 days on Trump’s tariff announcement and now OPEC accelerated production hikes.

USD CDX High Yield is now above 400bp. Last there in December 2023 when the S&P was close to 4,600 and NASDAQ 100 was at 16,000!

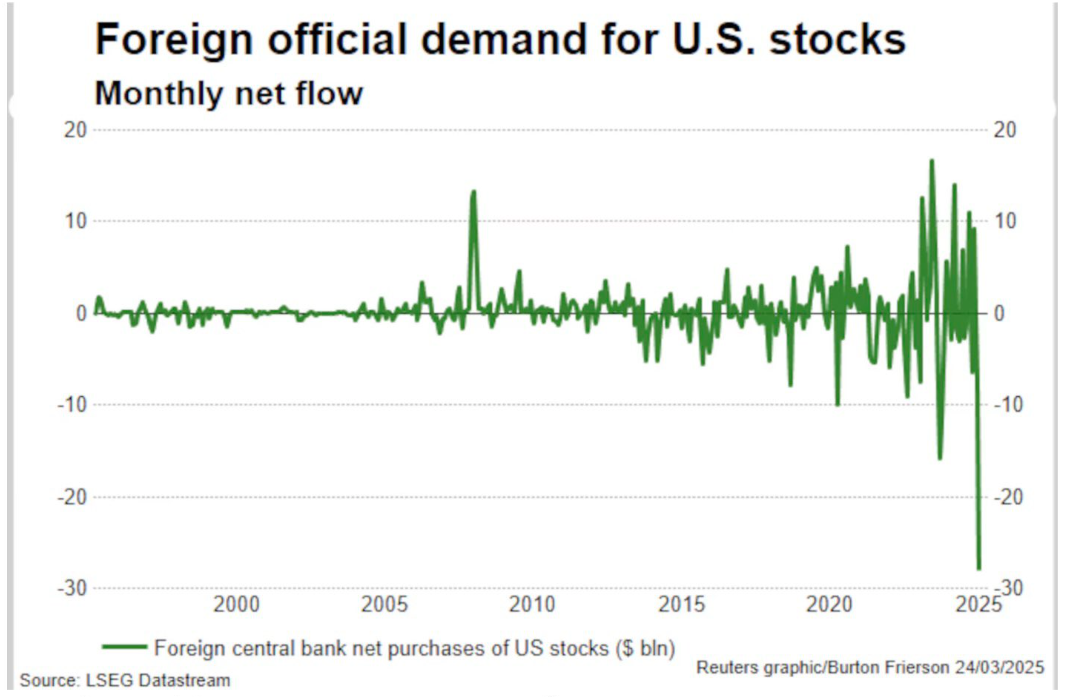

Foreign central bank demand for U.S. equities plummets (Chart 3, LSEG Datastream)

Data today – U.S. and Canadian employment data, both1.30pm BST.

Morning Macro 3rd April

Trump’s Liberation Day tariff announcement in the Rose Garden surprised the market, with reciprocal tariffs far higher than expectations (Chart 1, @Geiger_Capital).

U.S. equity futures immediately sold off 3% and wiped $2 trillion off US equity valuations in just 16 minutes. These are particularly hard on China and emerging markets with Chinese 10 yr yields down -8bps and the Vietnamese equities (46% tariff) down -6% this morning. The US 10-year yield (Chart 2, Bloomberg) has also broken key support as ‘risk off’ sentiment grips the market. The OIS is now pricing a 25% chance (and rising) of a rate cut at the upcoming 7th May meeting.

A recession is not confirmed if Trump finds a way to pressure countries to drop tariffs, but the flip side would be an escalation such as Chinese Yuan devaluation.

China urges US to immediately lift tariffs, vows retaliation – Reuters

*CHINA IS SAID TO RESTRICT COMPANIES FROM INVESTING IN THE U.S.

ADP employment surprised to the upside. This has a low correlation with payroll but still surprising based on the ISM employment data. ADP chief economist: “Despite policy uncertainty and downbeat consumers, the bottom line is this: The March topline number was a good one for the economy and employers of all sizes…” and especially good for the manufacturing sector.

*TRUMP SAID MUSK WILL STEP BACK FROM CURRENT ROLE ‘IN COMING WEEKS’: POLITICO

Data today – US jobless claims & ISM services, EZ PPI

Morning Macro 2nd April

As Liberation Day finally arrives U.S. economic data was significantly worse than expected yesterday with ISM manufacturing, new orders and employment falling much harder than expected while prices paid jumped to the highest levels since June 2022. More stagflation concerns for the Federal Reserve.

The White House says President Trump has “made up his mind” on tariffs which will likely be announced on April 2nd at 4 PM ET. While ISRAEL ELIMINATES TARIFFS ON US GOODS, PM OFFICE SAYS……Vietnam follows suit too.

ISM Manufacturing 49.0, Exp. 49.5, Last 50.3

New Orders 45.2, Exp. 48.4

Employment 44.7, Exp. 47.2

Prices Paid 69.4, Exp. 64.6 HIGHEST SINCE JUNE 2022

*US FEB. JOB OPENINGS 7.568M; EST. 7.658M

A bounce in Chicago regional PMI but still in contraction. US CHICAGO PMI ACTUAL 47.6 (FORECAST 45, PREVIOUS 45.5)

Recession in Germany is getting WORSE: 2,922,000 people are unemployed in Germany, the most since June 2020 peak of 2,930,000. This is the 2nd-highest level in 11 YEARS. The unemployment rate rose to 6.3% in March, the highest since July 2020 of 6.4%.

Everyone expects U.S. equities to fall, but no one is trading it. (Chart 1, Zerohedge), while CTAs remain short with $30B exposure.

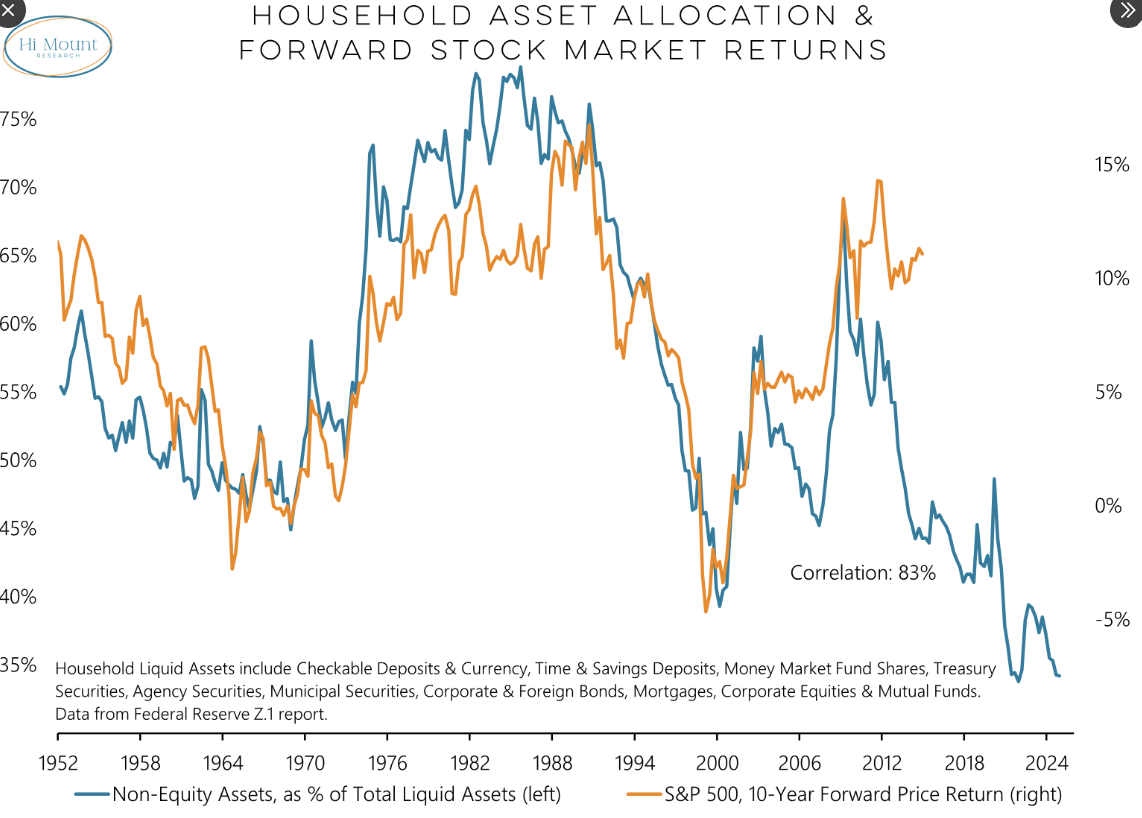

A similar breakdown in the correlation between consumer sentiment and equity exposure (Chart 2, Hi Mount Research)

Likewise the recent CDS move implies equities should be lower as well (Chart 3, 5y HY CDS inverted vs S&P500, Bloomberg)

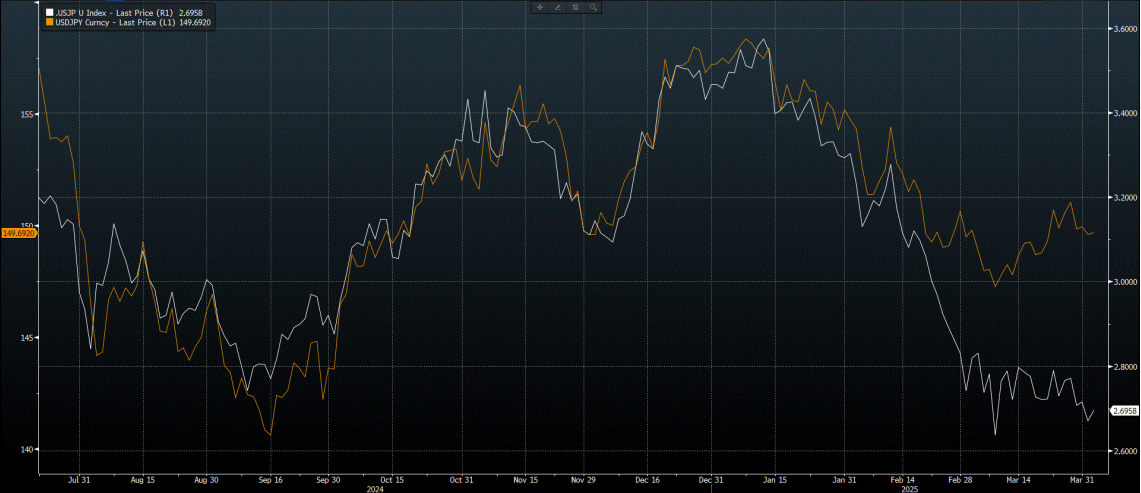

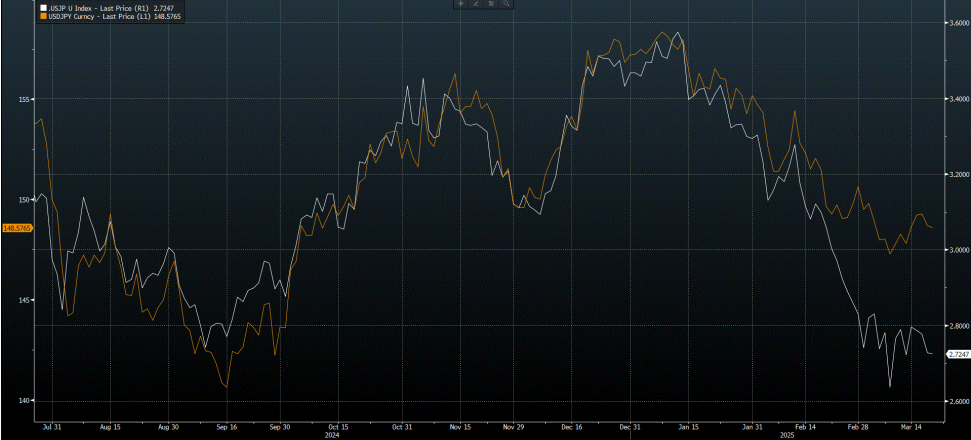

Meanwhile USDJPY is ignoring the recent moves in interest rate differentials (Chart 4, USDJPY vs 2yr IRS differential, Bloomberg)

Data today includes US mortgage applications, ADP employment, but will be overwhelmed by Trumps Rose Garden Liberation Day speech.

Morning Macro 1st April

Gold, new all-time high (not an April fools joke!)

China Caixin PMI Manufacturing Mar: 51.2 (est 50.6; prev 50.8)

Reserve bank of Australia unchanged at today’s meeting ….. RTRS – RBA GOV BULLOCK: BOARD DID NOT DISCUUSS A RATE CUT

On a quiet day for data, another poor U.S. regional survey, very much secondary data but similar signals across all regions. Dallas Fed Manufacturing Index fell to -16.3 for a second consecutive monthly decline (estimated -5.0). It was pulled down by a drop in the growth rate of new orders and employment. Uncertainty index rose sharply. (Chart 1, Bloomberg)

German inflation eased slightly in March. The headline inflation rate fell from 2.3% in Feb to 2.2%, while core inflation (excluding energy & food) dropped from 2.7% to 2.5%.

U.S. stocks continue to underperform (Chart 2, Bloomberg)

With a big week of employment data ahead the Challenger job cuts data suggest a sharply weakening job market (Chart 3. Steno research, Bloomberg & Macrobond)

Data today – EZ CPI, US ISM Manufacturing, and JOLTS job opening

Morning Macro 31st March

A whiff of panic in the air Monday morning. Gold up another 1%, Nikkei down -4.1%, Nasdaq futures down -1.3%, US 2s and 10s yields down another 8 basis points. Over the weekend economists are suddenly upgrading their recession probabilities and Liberation Day arrives this Wednesday. But most concerning for the market credit spreads are suddenly ripping higher which will drag risk lower (Chart 1, @AlessioTMAD)

*TRUMP TEAM WEIGHS BROADER, HIGHER TARIFFS: WSJ

China Manufacturing PMI Mar: 50.5 (est 50.4; prev 50.2) –

Non-Manufacturing PMI: 50.8 (est 50.6; prev 50.4) –

Composite PMI: 51.4 (prev 51.1)

Despite significant falls in interest rates Chinese household borrowing growth has slowed to less than 3% YoY. In contrast deposits continue to grow strongly. Effective delevering => disinflation/deflation.(Chart 2, @PPGMacro)

6.1 million Americans are behind on their mortgage.(Chart 2)

Goldman’s Kostin just slashed his 3M and 12M S&P forecasts again, to 5300 and 5900. 3 weeks ago this was 6500…………. Amazing what lower prices do!

Data this week

Monday – Chicago PMI

Tuesday – Japanese Tankan & unemployment rate, EZ inflation, US ISM manufacturing PMI & JOLTS

Wednesday – US mortgage applications, ADP employment

Thursday – China Caixin PMI, US ISM services PMI

Friday – US payrolls

Morning Macro 28th March

Gold makes more all-time highs $3,086, while Asian stocks were pressured again overnight, Nikkei -1.8%, HS Tech -1.5% and Bitcoin -2.5%.

Macron on Trump Tariffs: Europeans will respond by reciprocating.

Canada’s Carney was blunt. “The old relationship we had with the United States—based on deepening integration of our economies and tight security and military cooperation—is over.”

France March preliminary CPI +0.8% vs +0.9% y/y expected, with PPI -1.4% y/y.

US 1yr inflation swap makes a new high, inflation (tariff) fears continue growing. (Chart 1, Bloomberg)

Tokyo March Core CPI Rises 2.4% Year on Year; Est. +2.2%…. Yen strengthens, along with equity ‘risk off’ sentiment.

High year spreads starting to break higher, watch this red flag closely, ‘risk off’ warning. (Chart 2, Michael J.Kramer)

UK retail sales for Feb, +1.0% m/m (est. -0.3%) +2.0% y/y. Two months in a row of encouraging data and volumes actually picking up. (Chart 3) This goes against the current narrative of weakening UK consumer.

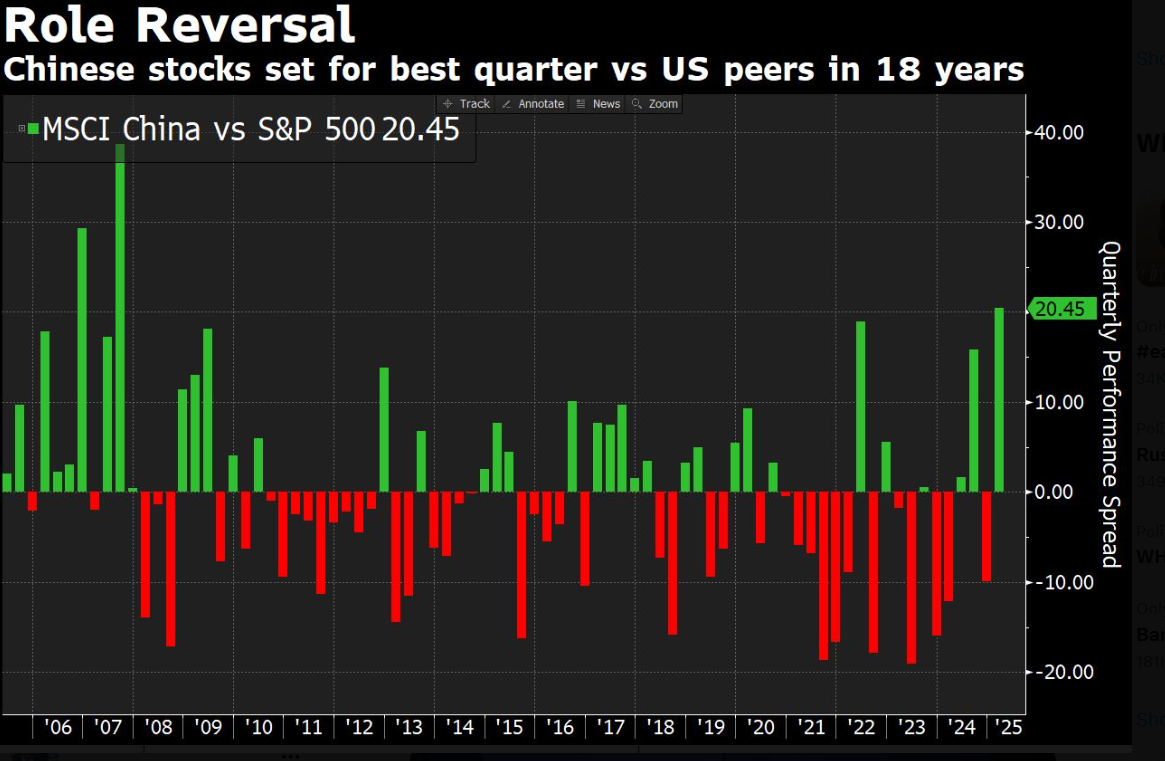

Chinese stocks set for best quarter vs S&P 500 in 18 years (Chart 4, Bloomberg David Ingles TV).

A slowdown coming in global semiconductor sales and more pain ahead for US IT company profits overall. (Chart 5, The Daily Spark, Torsten Slok from Apollo)

Data today – German GfK Consumer Sentiment & Unemployment Rate, EZ Sentiment, and key US core PCE price index (Personal Consumption Expenditure, the Fed’s ‘favoured’ inflation measure)

Morning Macro 27th March

TRUMP: PEOPLE WILL BE PLEASANTLY SURPRISED ABOUT RECIPROCAL TARIFFS – Reuters News

TRUMP: RECIPROCAL TARIFFS ON APRIL 2 WILL BE ON ALL COUNTRIES*TRUMP ANNOUNCES 25% AUTO TARIFFS ON ALL CARS NOT MADE IN US

Trump: If EU works with Canada to do harm, more tariffs coming

Trump: Plans higher tariffs if EU works with Canada against US

Trump administration hits China with slew of tech export controls – Nikkei

……. Japan says ‘every option’ on the table against Donald Trump’s 25% car tariffs.

*U.S. BLACKLIST OVER 50 CHINESE COMPANIES IN BID TO CURB BEIJING’S AI, CHIP CAPABILITIES…..

MICROSOFT CANCELS OR POSTPONES 2GW OF DATA CENTER PROJECTS AMID AI INFRASTRUCTURE OVERSUPPLY CONCERNS.

AI MARKET SHIFTS LEAD MICROSOFT TO SCALE BACK NEW BUSINESS WITH OPENAI DESPITE ITS $13 BILLION INVESTMENT.

Nasdaq fell 1.8%. TECH STOCKS, INCLUDING MICROSOFT AND NVIDIA, DIP AS INVESTORS WORRY ABOUT AI INFRASTRUCTURE GROWTH SLOWDOWNS.

The differential between CME Copper and London Copper is by far the largest in history. Appears tariffs are inflationary. (Chart 1, Bloomberg).

Both Toyota and General Motors are taking a dive after Trump’s announcement of 25% tariffs on cars manufactured outside the US. But Tesla stock unmoved by the announcement. (Well who’d have thought!)

Other than during the Pandemic, the Atlanta Fed’s GDPNow has never been weaker than its recent forecasts. It might not be the best forecaster but if it’s even in the right ballpark……. (Chart 2, Bloomberg)

Yet despite the weak regional Fed survey we get a strong durable goods orders. Rarely do I remember so much conflicting data. The main takeaway I think is the rear-view data remains resilient, the forward looking data incorporates tariff fears…

Durable goods 0.9%, Exp. -1.0%

Durables ex transports 0.7%, Exp. 0.2%

Cap goods shipments nondef ex air 0.9%, Exp. 0.2%

Cap goods orders nondef ex air -0.3%, Exp. 0.2%

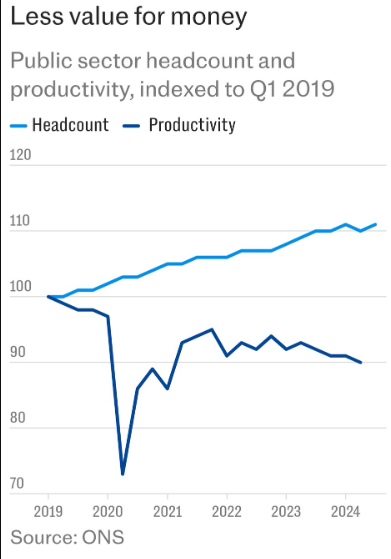

The shocking performance of the public sector in the UK. Number of HR staff in the Civil Service is up 62% since 2019. (Chart 3, ONS. PPGMacro)

Data today – US GDP & PCE Final (Q4), Jobless Claims

Morning Macro 26th March

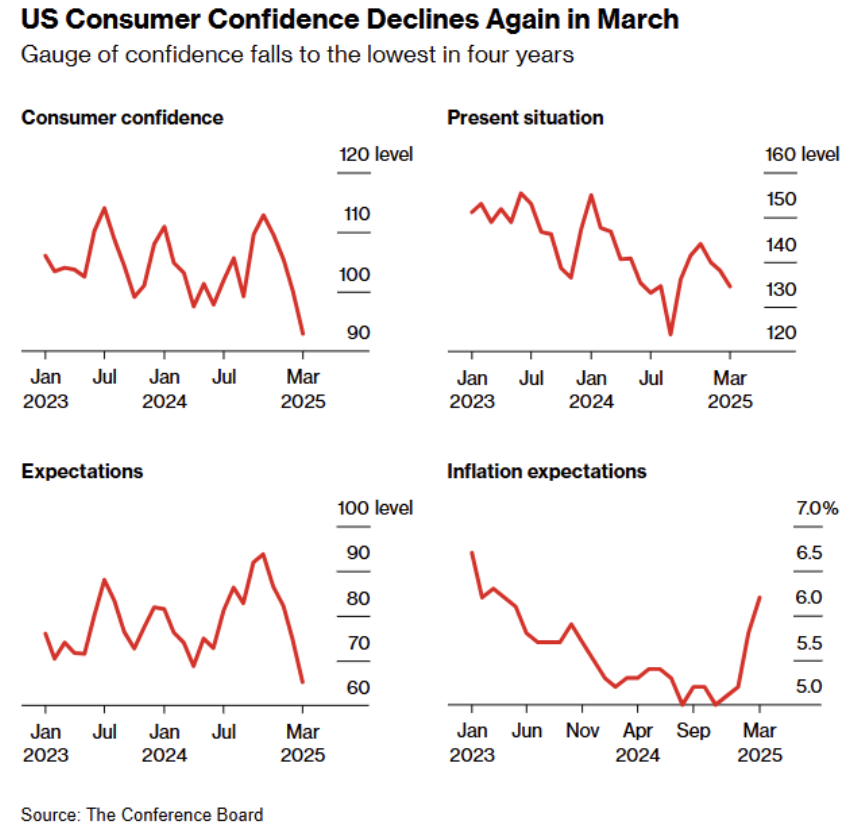

U.S Conference Board’s consumer confidence reading fell sharply with expectations the lowest since 2013. (Chart 1). The headline reading collapsed more than expected from 100.1 to 92.9 (exp 94.4). While the average 12-month inflation expectations rose again, from 5.8% in February to 6.2% in March. More headaches for the Federal Reserve.

And the most watched regional survey the Philadelphia Fed services index drops to its lowest level since the pandemic. But this is a manufacturing hub, and as we saw from the flash PMI’s on Monday the US service sector remains resilient keeping the composite PMI’s above 50 and consistent with steady GDP (Chart 2)

German business optimism rose to the highest level since June 2024. In the big picture it’s marginal improvement, but improvement all the same. (Chart 3)

Trump added to the tariff confusion before next weeks April 2nd implementation, pledging levies on cars in the coming days while indicating nations will receive breaks from next week’s “reciprocal” duties. He’s also proposing a 25% fee on any nation purchasing oil and gas from Venezuela.

US lay-off announcements are surging (Chart 4, BCA research)

Stock market returns tend to follow liquidity. Household non-equity liquidity finished 2024 near an all-time low. (Chart 5, Hi Mount research)……

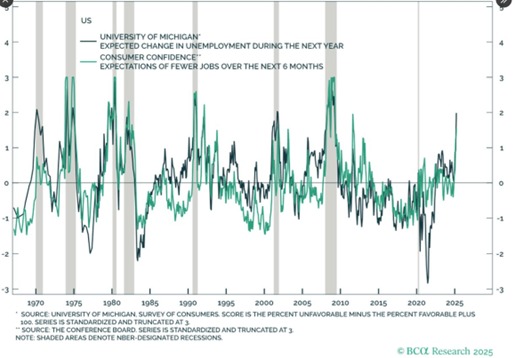

….. Expectations of rising unemployment surging in both the University of Michigan and Conference Board surveys. (Chart 6 , BCA research)

Chinese yields are now trending lower. 10-year gov’t bond peaked last week at 2%, and now trades 1.87%, as key stock markets CSI300 and Hang Seng are also heading lower.

Meanwhile Japanese 2yr and 10yr gov’t bonds make new cycle highs on BOJ governor Ueda’s comments. “If the economic and price outlook outlined in the (BOJ) Outlook Report is realized, we will continue to raise policy interest rates and adjust the level of monetary easing,” Ueda told the parliament.

UK inflation comes in slightly lower than expectations and last months print (+0.4%m/m, 2.8% y/y, est +0.5% and 2.9%). A bit of relief for the BOE, before Rachel Reeves spring budget today.

A staggering chart that will scare European car makers (again). (Chart 7)

Moody’s: US fiscal strength deteriorated further since the rating agency assigned a Negative outlook to the US sovereign rating.

BYD revenue $107B, growing at 27% per year, and rapidly gaining market share… valued at $160B. While Tesla revenue $98B, growing at 1% per year, and rapidly losing market share… valued at $900B. One is cheap and one is expensive, go figure.

No key data today, just headline risk!

FT Commodities Summit: CCI CEO, William C. Reed II – ‘Tariffs are destabilizing’. he said he is expecting prices for commodities to rise and spark inflation. ‘It will be very hard for people with a fixed income,’ he added but was not ready to commit to an expected number as ‘there are many other things like monetary policy.’ he thought the US needs to be ready to fight a war and needed to be prepared to have all it need it to fight it.

FT Commodities Summit: Torbjörn Törnqvist, Co-Founder and Chairman at Gunvor, when asked what is the impact of Trump’s actions, Torbjorn surprisingly said, ‘nothing.’ He said that the sanctions do not change in the balances as supply and demand remain unchanged. Prices were they are -70s- is a fair price, he concluded.

FT Commodities Conference: Jeff Currie opens the Energy Transition panel and states that transition is not about lowering a green footprint but setting an energy independence path. He said that the order should be security, affordability and the environment in that order. And any other ordering would lead to troubles

Morning Macro 26th March

‘Risk on’ sentiment with rumblings of some countries avoiding April 2nd tariffs and better than expected flash PMI data (Purchasing Manager Index). The ‘risk on’ sentiment saw the dollar rally for the 5th consecutive day, EURUSD now trades 1.0777, from last week’s high 1.0955, and U.S. 2yr and 10yr yields rally 9 basis points. Equities bounced with the Nasdaq up 2.2% and the S&P 500 up 1.8%. Meanwhile the gold uptrend stalled currently trading $3,014 from last week’s $3,057 high….

TRUMP: I MAY GIVE A LOT OF COUNTRIES BREAKS ON TARIFFS .…

U.S. MARCH SERVICES PMI RISES TO 54.3, EXP. 51.2, LAST 51.0

U.S. MARCH MANUFACTURING PMI FALLS TO 49.8, EXP. 51.9

PMIs surged to a seven-month high in the Eurozone, and a six-month high in the UK.

Hang Seng market turns bearish, down another 3.8% today.

Fed’s Bostic: We won’t get back to 2% inflation until early 2027.

TRUMP: ANY COUNTRY BUYING VENEZUELA OIL TO FACE 25% U.S. TARIFF

US Treasury Secretary Bessent: Interest rates are going to keep declining as energy costs decline.

Slowly, slowly, more pressure on the Federal Reserve TRUMP: I WOULD LIKE TO SEE THE FED LOWER INTEREST RATES

Tesla – having sold off 55% from the highs, Tesla rallied 5.3% yesterday and is up 11.7% today pre-market……meanwhile Cathie Wood sees Tesla hitting at $2600 (it’s currently at $278).

As the BOJ mulls asset sales just a reminder the BOJ owns over 7% of the Japanese stock market ~ 500B USD worth in ETF’s. That’s a lot of potential supply.

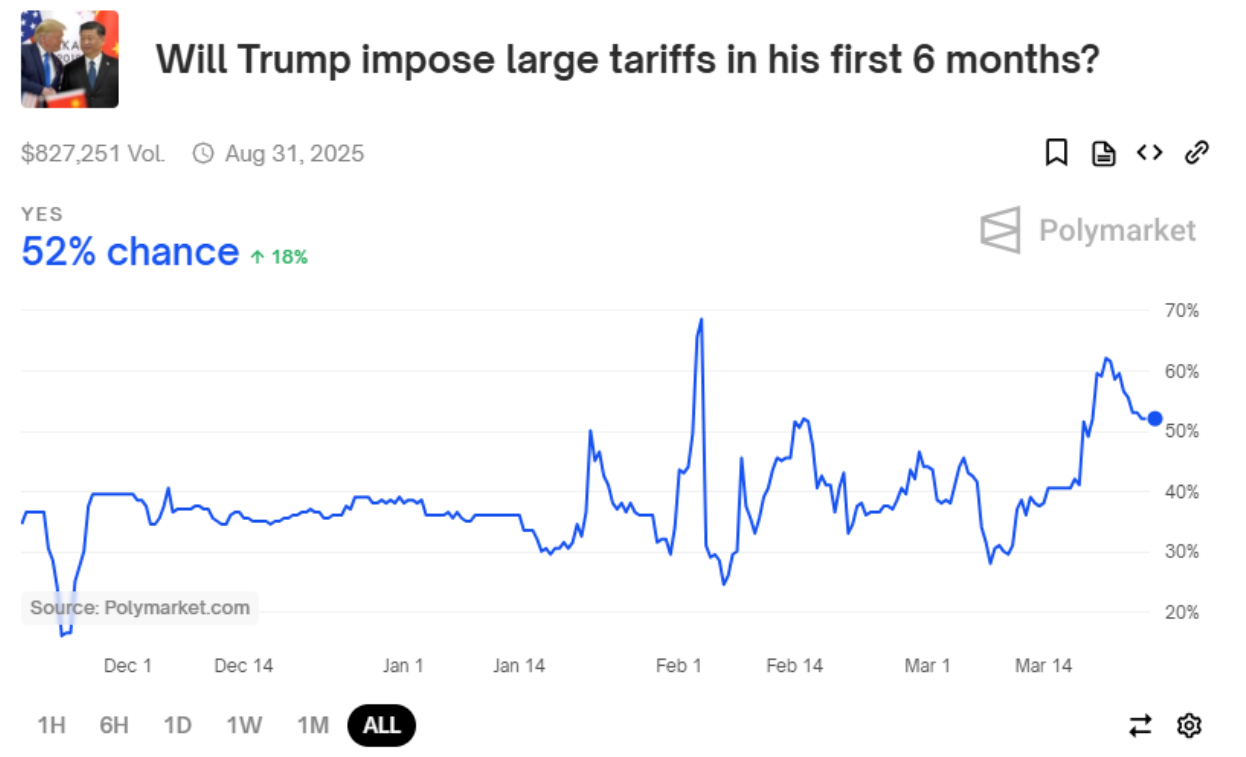

Meanwhile expect another week full of headline risk, as Polymarket sees Trump imposing large tariffs still just above 50:50.

Key data today – German IFO, US new home sales & consumer confidence

Morning Macro 24th March

More tariff flip flopping…. Just a few hours after Trump tweets April 2nd, “LIBERATION DAY IN AMERICA!” we get a step back reported in the Wall St Journal which sends risk higher to open the week….

WHITE HOUSE SCALES BACK APRIL 2 TARIFF PLAN, FOCUSES ON TARGETED RECIPROCAL LEVIES – WSJ || SECTORAL TARIFFS ON CARS, CHIPS, PHARMA UNLIKELY TO BE ANNOUNCED APRIL 2 || RECIPROCAL TARIFFS STILL SET TO HIT TOP TRADING PARTNERS INCLUDING ‘DIRTY 15’ || CANADA, MEXICO, EU AMONG NATIONS FACING HIGHER DUTIES; EXEMPTIONS LIMITED.

ECB’s Cipollone: Inflation target may be reached sooner than last projections indicated.

Turkey’s stock market saw its worst week in 17 years. On Sunday, Turkish regulators imposed a ban on short-selling and relaxed buyback rules.

Barclays says further PBOC easing is becoming increasingly unavoidable. Analysts at the bank point to low inflation, muted domestic demand, and growing tariff tensions.

Data this week

Monday – EZ, UK, US Flash PMIs

Tuesday – German IFO, US new home sales & consumer confidence

Wednesday – Australian CPI, UK CPI

Thursday – Japan Tokyo CPI, US jobless claims, GDP Q1F, pending home sales

Friday – UK retail sales, US UMich sentiment, Core PCE Deflator

Morning Macro 21st March

The dollar finally finds some buyers and rallies back above 104.00.

US President Trump signed an order to increase the production of critical minerals.

US CEO confidence has officially dropped to its lowest level in 13 years, falling 5 points over the last month. This marks the largest monthly decline in the history of the poll, according to Chief Executive Magazine surveying 220 US CEOs. The current business conditions assessment dropped 20%, to 5 points, the lowest since 2020. Furthermore, economic outlook for the next 12 months fell 28% to the lowest since November 2012. Only 39% of respondents now believe the business climate will improve this year, down from 52% at the beginning of the year. At the same time, 36% expect things to get worse, up from 20% in January.

Conference Board’s Leading Economic Index fell by 0.3% m/m in February … third consecutive decline and largest drop since last October. (Chart 1, Bloomberg).

New York business services activity dropped 8.8 points in March, to -19.3, (Chart) the lowest since January 2023. The index of expectations fell 24.9 points, to -3.3, its lowest since December 2022. The business climate index fell 16.0 points, to -51.7, its lowest in 4 years…… while March Philly Fed Manufacturing Index also fell to +12.5 (est +9. last +18.1) … new orders and shipments eased from prior month but remain in expansion; workweek accelerated alongside employment (which is at highest since October 2022).

UK February inflation expectations for the year ahead 3.9% vs 3.5% prior, as the BOE kept rates on hold with a hawkish statement. They expressed concern around the rate of disinflation, but this should be negated by the deteriorating economic outlook. A tough outlook for the central bank…… Meanwhile the UK OBR (Office for Budget Responsibility) halved its UK growth forecasts and announced the government is overshooting on the ‘current budget’. Borrowing in the financial year to February 2025 was £20.4 billion more than the £111.8 billion forecast by the OBR last October.

Japanese CPI come is at +3.7% (est 3.5%), lower than previous month but above estimates and 1% above U.S. Yield differentials favouring the Japanese Yen currency again.

Weak Aussie employment data -58k (est +30k) saw the Aussie dollar and Australian yields fall.

Weak German PPI -0.2% m/m (+0.7% y/y, est +1.0% y/y)

*SWISS CENTRAL BANK CUTS KEY INTEREST RATE BY 25BPS TO 0.25%, LOWEST SINCE JUNE 2022…. And a surprise to the market.

Chinese stocks and yields have turned lower while economic momentum in South Korea and Indonesia is now slowing.

Headwinds for iron ore – China’s steel industry is considering paying firms to shutter outdated steel plants, amid government efforts to rein in the country’s mammoth output https://bloomberg

Is this really allowed?. Commerce Secretary Howard Lutnick on Tesla: Lutnick urged the public to buy Tesla shares, calling them “unbelievably cheap” and saying, “It’ll never be this cheap again.”

No key data today.

Morning Macro 20th March

A very dovish Fed sees the 2-year yield fall 14bp from its high and equities rally (Nasdaq +1.3%), gold rally and cross-Yen currencies fall. They revised growth lower, both unemployment & inflation higher and reduce the balance sheet run off form 1st April……

Powell did say “The economy is strong overall”, “Recent indications point to moderation in consumer spending” and there is “Heightened uncertainty about business outlook” while playing down the inflation risk “Inflation was transitory the last time there were tariffs.” …….

However, the Fed now appears data driven (which is backward looking, amid plenty of Tariff uncertainty, and while the Fed dot plots project 50bp of cuts this year and next, the OIS is pricing 64bp of cuts this year and looking for more…….

Fed cuts year-end GDP forecast from 2.1% to 1.7%

Fed raises year-end core PCE forecast from 2.5% to 2.8%

Fed raises year-end unemployment forecast from 4.3% to 4.4%

TRUMP: If the Fed isn’t going to cut, I’m going to make them want to cut.

TRUMP AIDES PREP NEW TARIFFS ON IMPORTS WORTH TRILLIONS FOR ‘LIBERATION DAY’ – WAPO

US-Japan yield differentials suggest USDJPY has plenty of room to go lower (Chart 1)

Gold new all-time high!

Copper hits $10,046.50 per ton, driven by U.S. tariff fears, supply shortages, and green energy demand (Chart 2, Bloomberg)

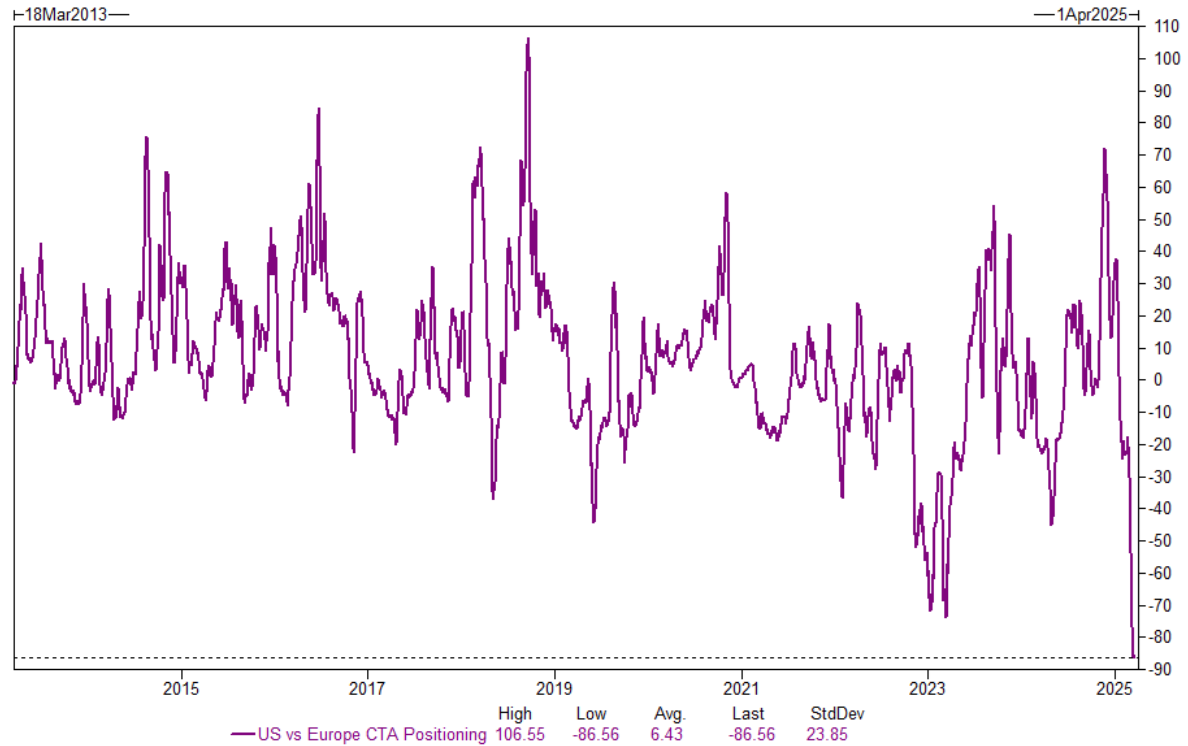

“CTAs are short -$34bn of US equities vs long $52bn of European equities … that spread is the largest we have ever seen by a decent margin” – Goldman Sachs (Chart 3, Goldman Sachs)

And while we’ve recently highlighted the massive spike in supply of US family homes for sale mortgage applications are up 27% y/y. Backward looking data but still signalling rates are not restrictive for the housing market at these levels (Chart 4, Bloomberg)

UK labour market data, but mostly reassuring… headline unemployment stable at relatively low 4.4%, payrolled employment little changed regular pay growth in the private sector holding above 6% (though this may be too hot for the BoE) . However these are lagging indicators for January and February, the forward-looking surveys are much weaker.

Euro-area inflation slowed more than initially reported, strengthening the case for the European Central Bank to lower borrowing costs.

Amazon eyes sales of used cars – Automotive News | Probably not a positive for used car dealers trading at 100x EPS, with record margins.

*TURKEY’S MAIN STOCK INDEX PLUNGES ALMOST 7% AMID POLITICAL DRAMA.

Data today – Bank of England policy meeting (no change in rates expected), US jobless claims, Philly Fed data, Leading indicators & Existing home sales. Canada PPI, Japanese CPI overnight.

Morning Macro 19th March

Gold makes yet another all-time high. A steady & continuous uptrend. But noticeably the BofA Global Fund Managers Survey does NOT see it as a crowded trade. (Chart 1, BofA Global Research)

While retail buy stocks hedge funds have record rotation out of US stocks. (Chart 2, BofA Global Research)

Investment cycles. Note the slowdown in investor sentiment (Chart 3, BofA Global Research)

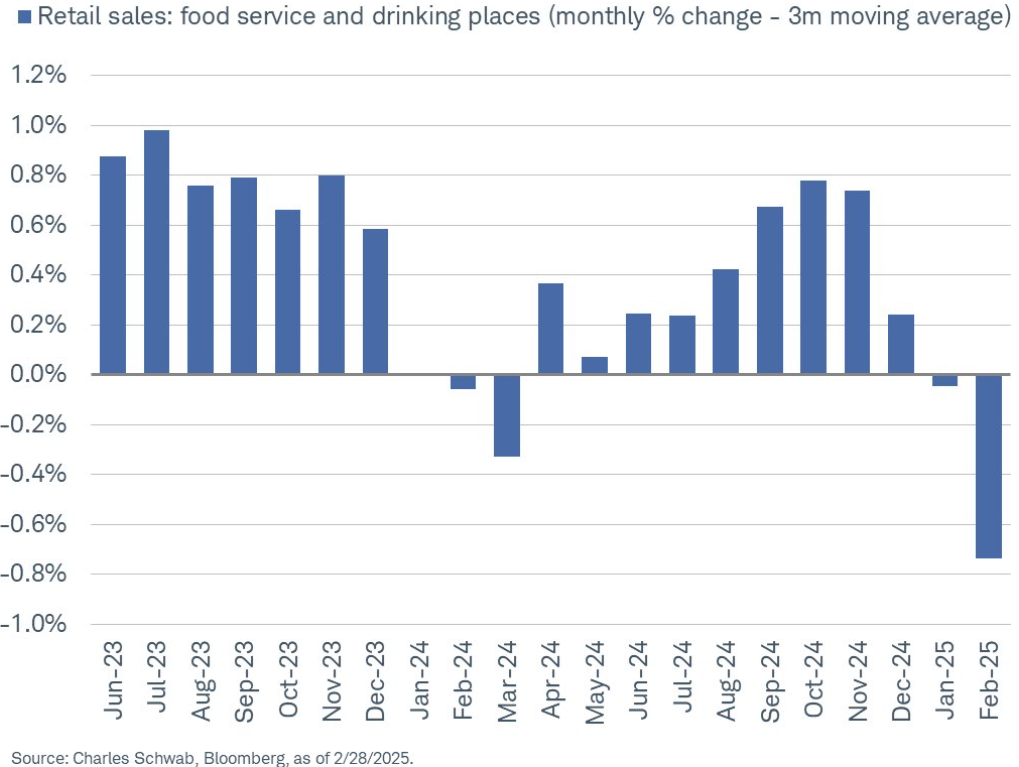

U.S. real data showing negative economic outcomes… 3m average of restaurant and bar retail sales growth fell sharply and further into negative territory in February. (Chart 4, Charles Schwab, Bloomberg)

While consumer sentiment data highlights rising inflation concerns US breakeven inflation rates continue falling (nominal yield minus TIPS yield).(Chart 5, Bloomberg, Goldman Sachs Investment Research)

Tesla closes down -54% from its all-time high.

Mag 7 -20.6% over the past 60 days … only two periods that saw that kind of decline (or worse): late-2018 and 2022

Amazon Undercuts Nvidia With Aggressive AI Chip Discounts.

Yesterday Indonesia stock exchange circuit breaker, trading halted as market down -5%. Later trading as much as 7.1% on Tuesday, marking its biggest intraday slump since 2011.

Bloomberg: “Chinese banks are slashing rates on consumer loans to record lows as policymakers ramp up stimulus to stabilize growth and counter US President Donald Trump’s tariffs.”……….Meanwhile Chinese 10-year bond continues its uptrend, 1.97% (from 1.60% double bottom in Jan/Feb). The market continues to price economic recovery.

BOJ unchanged today….. meanwhile Japan’s and prices rise at strongest pace in 34 years – Reuters

FOMC tonight, Overnight Index Swap pricing no change, but the market will closely listen to Powells press conference.

Morning Macro 18th March

Headline US retail sales are weak, but the control group strong. Bottom line is real retail sales volume has moved sideways for 2 years and is starting to now decline (Chart 1 EPBResearch)

US Retail Sales Advance (M/M) Feb: 0.2% (est 0.6%; prev -0.9%)

Retail Sales Control Group (M/M): 1.0% (est 0.3%; prev -0.8%)

More signs of a sharp slowdown in U.S. regional data….. NY FED MANUFACTURING ACTUAL -20 (FORECAST -1.9, PREVIOUS 5.70). …….. While prices paid and received rose sharply.

Two strong sessions in S&P. Back-to-back large volume upside days (86% and 91%). Six prior instances of back-to-back >85% days since 2009, all of them bearish towards a retest of the recent lows.

JP Morgan expects Tesla to report its worst quarterly deliveries in three years: “We struggle to think of anything analogous in the history of the automotive industry, in which a brand has lost so much value so quickly.”

US high-yield corporate bond spreads are up ~60 basis points over the last month, to 3.20%, a 6-month high. At the same time, investment grade corporate bond spreads have risen 27 bps, to 0.96%, the highest since September 2024. Corporate bond spreads are a good barometer of risk (financial market distress). These are still low levels but moving in the wrong direction.

Warren Buffett has boosted his stake in Japan’s big trading houses to ~10%. Mitsubishi, Marubeni, Mitsui, Itochu, and Sumitomo. These are among world’s top investors in natural resources.

Israel’s military conducted extensive strikes on targets belonging to Hamas in Gaza. Based on reports Hamas was preparing another attack.

USDJPY rally with yields/equities bouncing seems to have got ahead of the interest rate differentials (Chart 2 USDJPY vs 2yr IRS differentials)

Australian Consumer confidence dives 3% to be back to its lowest point since October 2024.

Behind the tariff/Ukraine/DOGE headlines, risk to the U.S. housing market continues to rise. Here US new one family houses for sale continues to rise close to the pre-GFC peak (Chart 3)

Data today – German/EZ ZEW, Canadian Inflation, US Industrial Production, German Bundestag third reading on fiscal reform (vote), US President Trump-Russian President Putin Call.

Morning Macro 17th March

China data beats expectations (all but housing)

*CHINA JAN.-FEB. RETAIL SALES RISE 4% Y/Y; EST. 3.8%

*CHINA JAN.-FEB. FIXED INVESTMENT RISES 4.1% Y/Y; EST. 3.2%

*CHINA JAN.-FEB. INDUSTRIAL OUTPUT RISES 5.9% Y/Y; EST. 5.3%

Also China has just announced the “Consumption Boosting Action Plan”, pledging to “vigorously boost consumption and comprehensively expand domestic demand”. The plan encompasses eight major initiatives:

Income Growth & Employment Support – Policies to increase wages, stabilize employment, strengthen financial markets, and support rural incomes.

Stronger Social Safety Net – Enhancements to child-rearing subsidies, pensions, healthcare coverage, and social assistance programs.

Upgraded Service Consumption – Expansion of elderly care, childcare, tourism, entertainment, and sports offerings, along with broader visa-free access for inbound travelers.

Big-Ticket Purchases & Housing Market Stability – Incentives for trade-ins on cars, home appliances, and electronics, as well as measures to stabilize the real estate market.

Consumption Quality & Innovation – Promotion of premium domestic brands, digital consumption, AI-driven services, and emerging consumption models.

Consumer Protections & Market Access – Strengthened consumer rights protections, credit mechanisms, and regulatory reforms to stimulate spending.

Reducing Restrictions on Consumption – Streamlined approval processes and fewer bureaucratic barriers for major purchases and lifestyle services.

Policy & Financial Support – Coordinated fiscal and financial measures, including targeted subsidies, credit expansion, and investment in consumption infrastructure.

Economists now upgrading Chinese growth forecasts. ANZ bumps up China 2025 GDP growth forecast to 4.8% from 4.3% previously

JAPAN 40-YEAR YIELD INCREASES TO 3%, HIGHEST SINCE LAUNCH IN 2007.

TRUMP SAYS HE WILL BE SPEAKING WITH RUSSIA’S PUTIN ON TUESDAY

But while China improves U.S. data continues to disappoint…

U.S. Consumer sentiment–as measured by UMICH–continues to plunge.

UMICH Sentiment prelim Mar ’25 fell to 57.9 (63 consensus) from 64.7 in Feb, current conditions to 63.5 (64.4 cons) from 65.7, and Expectations to 54.2 (63 cons) from 64. Year ahead inflation expectations pop to 4.9% (4.3% cons) from 4.3%, while 5-year ahead expectations also jumped to 3.9% (3.4% cons) from 3.5%.

Germany’s CDU, SPD have agreed on a solution with Greens on financial package.

“Gold’s going to reach $4,000, says Gundlach. He also puts recession probability at 60%.” – Jeffrey Gundlach (The Bond King).

Data this week

Monday – US retail sales

Tuesday – EZ economic sentiment, US housing starts

Wednesday – BOJ & FOMC rate decision, NZ GDP

Thursday – BOE rate decision, Aussie employment, US leading index

Friday – US consumer confidence

Morning macro 14th March

A rumour is circulating in the A-share market that the PBOC may cut the reserve requirement ratio (RRR) after the release of financial data this afternoon, though it is still unclear whether the reduction will be 50 or 25 basis points.

Gold, new all-time highs (ground hog day) $2,992.

PPI deep freeze

PPI 0.0% MoM, Exp. 0.3%. PPI Core -0.1%, Exp. 0.3%

PPI 3.2% YoY, Exp. 3.3%. PPI Core 3.4%, Exp. 3.5%

Putin says Russia agrees to stop fighting in Ukraine, but it should lead to long-standing peace.

Pres. Trump threatens a 200% tariff on European wines, champagnes and alcohol. Donald Trump, “I’m not happy with the European Union, and we’re going to win that financial battle”

LUTNICK: EU RESPONSE TO US WAS DISRESPECTFUL

Portugal has cancelled the order for F-35s from the US and will replace their F-16s with European fighters. “We have to be able to count on the predictability of our allies, which is no longer the case with the United States.”

Tsy. Sec. Bessent on CNBC: “a ‘detox’ does not have to be a recession” and “The easy thing for us to have done, would have been to come in and just keep this massive spending going. But it’s unsustainable. Could we have kept it going for another 4 years? Yea maybe, but you’re risking financial calamity down the road.”

Investors are increasing worrying about US recession risks – and not just from DOGE cuts. Investors fear that now US pandemic-era household ‘excess saving’ is spent, the consumer is all tapped out.(Chart 1)

CTAs are now short -$18.6bn of US equities (0%ile rank) after selling $33bn over the last week.

As the S&P enters official correction, down -10% from highs, the Russell 2000 is now below levels 4 years ago. Mid cap America is really struggling.

Private equity getting slaughtered. (Chart 3)

The UK economy’s poor start to 2025 is confirmed in the official data… Monthly GDP fell 0.1% in January, against the consensus forecast of a 0.1% rise, led by the production sector (mainly due to falls in manufacturing output and oil & gas).

Japan’s Largest Trade Union Group Rengo: First-round data shows average wage hike of 5.46% for fiscal 2025 vs demand of 6.09% hike. Adding further pressure on BOJ to kike.

No key data today. Just random, unexpected Trump tweets!

Morning Macro 13th March

February CPI inflation FALLS to 2.8%, below expectations of 2.9%. Core CPI inflation FALLS to 3.1%, below expectations of 3.2%. This marks the first decline in both Headline and Core CPI since July 2024. Shelter dropping fast, but is still 55% of the rise of core CPI (MOM). The rapid drop will continue over next couple of months. Inflation is cooling down in the US.